MGIC Bundle

Who Does MGIC Serve in the Mortgage Landscape?

In the ever-shifting world of real estate, understanding the MGIC SWOT Analysis and its customer base is paramount. This exploration delves into the core of MGIC Company's business strategy, examining its customer demographics and target market. The insights are crucial for investors, financial professionals, and anyone seeking to navigate the complexities of the housing market.

MGIC's success hinges on a deep understanding of its target market, which includes homebuyers and lenders. This analysis will uncover the characteristics of MGIC's ideal customer, including their age range, income levels, and geographic location, providing a comprehensive MGIC customer profile analysis. Furthermore, we'll examine how MGIC uses data to understand its customers and tailor its risk assessment strategies in a dynamic market influenced by interest rates and evolving borrower needs.

Who Are MGIC’s Main Customers?

The primary customer segments for the [Company Name] (MGIC) are primarily divided into two main groups: mortgage lenders and the consumers seeking homeownership. MGIC operates as a business-to-business (B2B) company, offering private mortgage insurance to lenders and financial institutions across the United States, Puerto Rico, and Guam.

These lenders then serve a diverse range of consumers (B2C) looking to purchase homes, particularly those who may not meet the traditional requirements for a 20% down payment. MGIC's services allow these consumers, including first-time homebuyers and those with low-to-moderate incomes, to enter the housing market with down payments as low as 3%.

While specific data on the age, gender, income, or education levels of the ultimate borrowers isn't always detailed in recent reports, the focus on low-down-payment mortgages indicates a target market that includes younger individuals and families. These consumers are often working to build wealth through homeownership.

MGIC's target market includes a broad spectrum of homebuyers, with a significant portion being first-time buyers and those with low-to-moderate incomes. This is because private mortgage insurance makes homeownership more accessible by reducing the required down payment.

The company's primary target market consists of mortgage lenders and financial institutions. These lenders, in turn, serve a diverse group of consumers seeking homeownership. The focus is on providing mortgage insurance that allows borrowers to purchase homes with smaller down payments.

Economic conditions significantly influence MGIC's target market. For instance, higher interest rates often extend loan persistency, which benefits mortgage insurance policies. Understanding how economic factors affect the market is crucial for MGIC's strategic planning.

The private mortgage insurance market has remained relatively stable, with expectations for slight growth in 2025. The overall purchase market in 2024 was approximately $1.3 trillion, and Fannie Mae expects growth to $1.42 trillion in 2025, indicating ongoing demand from homebuyers.

Key Data Points

MGIC's financial performance and market position are crucial for understanding its customer base and target market. Analyzing the Competitors Landscape of MGIC provides additional insights into the competitive environment and market dynamics.

- In 2024, MGIC's new insurance written (NIW) was $55.7 billion, a substantial increase from $46.1 billion in 2023.

- The company's insurance in force reached over $295 billion, covering 1.1 million mortgages as of December 31, 2024.

- The private mortgage insurance market has remained relatively flat over the past two years at approximately $300 billion, with expectations for a slightly larger market in 2025.

- The overall purchase market in 2024 was approximately $1.3 trillion, and Fannie Mae expects growth to $1.42 trillion in 2025.

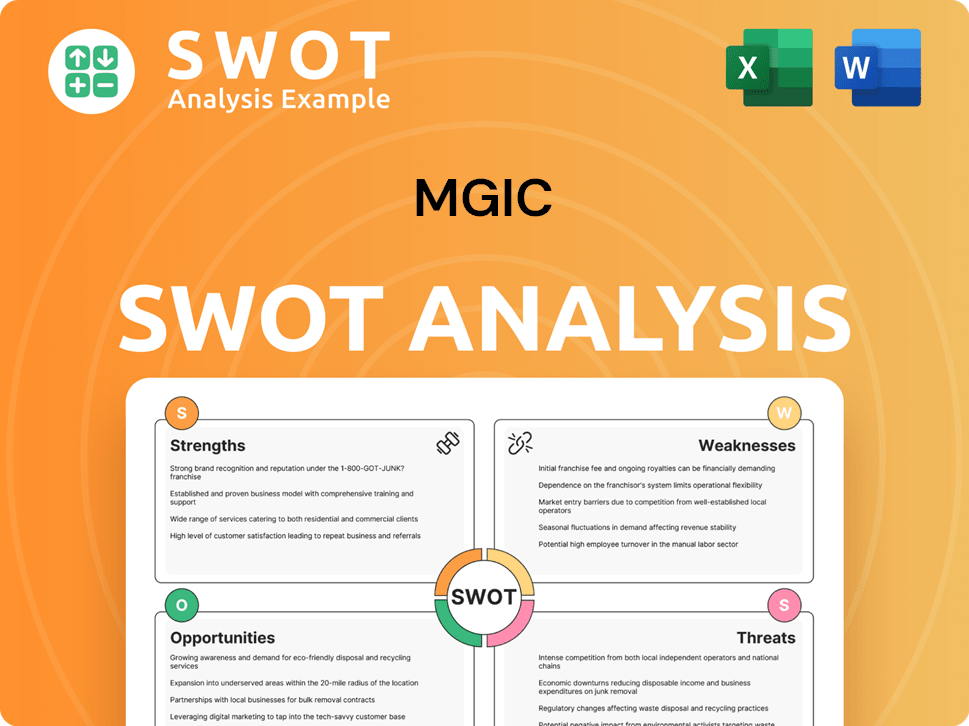

MGIC SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do MGIC’s Customers Want?

Understanding the customer needs and preferences is crucial for the success of the MGIC Company. The company's primary customers are mortgage lenders, and their main concern revolves around managing risk and facilitating homeownership. They seek to protect themselves from potential losses, especially with high loan-to-value (LTV) mortgages.

For the ultimate consumers, the ability to achieve homeownership sooner is the primary motivation for utilizing private mortgage insurance. This addresses the challenge of saving a substantial down payment, which can be a significant barrier to entering the housing market. Consumers are driven by the aspiration of homeownership and the associated economic and social benefits.

MGIC's approach involves insuring a portion of the mortgage loan, which makes it safer for financial institutions to originate loans with lower down payments. This allows lenders to expand their market reach to a broader segment of homebuyers. The company actively engages with loan originators to understand their needs and preferences, as seen in their 'Plan for 2025 with Insights from Originators' initiative, which dives into the results of a 2024 Loan Originators Survey.

Lenders' Needs

Lenders require protection against borrower default, especially for high LTV loans. They aim to expand their market reach to include more homebuyers. Their psychological driver is confidence in their loan portfolios.

Consumers' Needs

Consumers want to achieve homeownership sooner by reducing the down payment needed. They are motivated by the aspiration of homeownership and its benefits. This addresses the pain point of saving a large down payment.

MGIC's Response

MGIC provides mortgage insurance to mitigate risk for lenders. The company offers underwriting and risk management tools. They embrace new technologies like AI for fraud detection.

Market Trends

MGIC adapts to market trends and customer feedback. They use digital platforms and AI to meet evolving needs. Their initiatives show a commitment to understanding customer needs.

Customer Engagement

MGIC actively engages with loan originators. The 'Plan for 2025' initiative highlights this. This engagement helps them better serve end consumers.

Technological Advancements

MGIC utilizes digital mortgage insurance platforms. They leverage artificial intelligence for fraud detection. These technologies improve underwriting processes.

The company's focus on customer needs is evident in its product development and service offerings, including analytics and risk management tools. MGIC also incorporates new technologies, such as digital mortgage insurance platforms and AI, to meet evolving customer needs and improve underwriting processes. For more insights, consider reading a Brief History of MGIC.

Key Customer Needs and Preferences

MGIC's success hinges on understanding the needs of both lenders and homebuyers. Lenders require risk mitigation and market expansion, while homebuyers seek easier access to homeownership. The company's commitment to technology and customer engagement further enhances its ability to meet these needs.

- Lenders: Risk mitigation, market expansion.

- Homebuyers: Easier homeownership, reduced down payments.

- MGIC: Technology adoption, customer engagement.

- Market Trends: Digital platforms, AI for fraud detection.

- Customer Feedback: Influences product development.

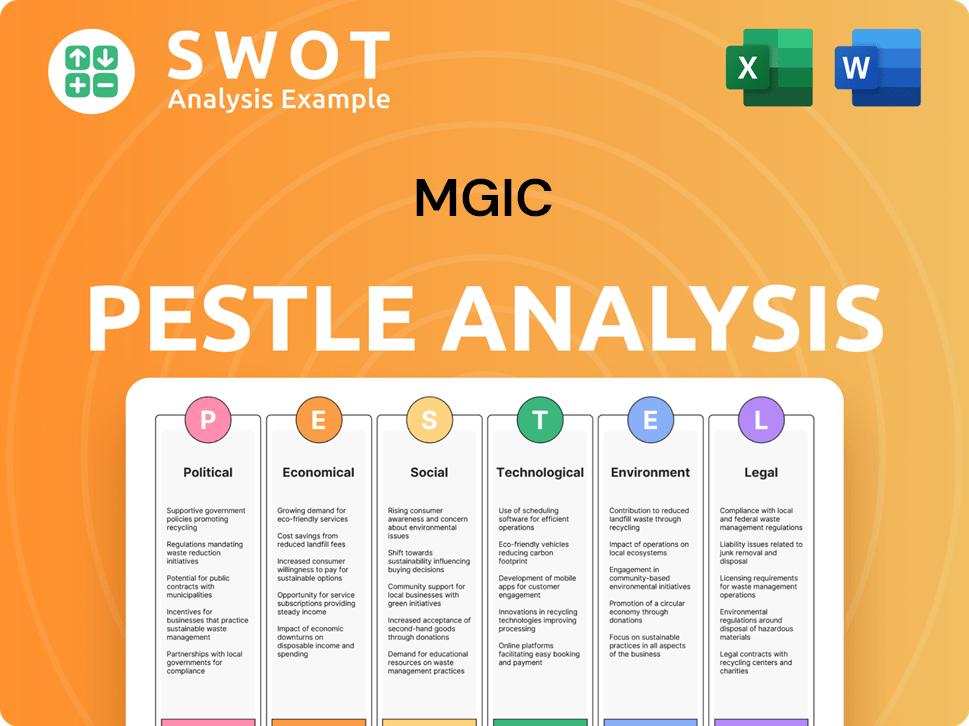

MGIC PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does MGIC operate?

The primary geographical market for MGIC Company is the United States. It operates as a leading provider of private mortgage insurance within the country. The company also extends its services to lenders in Puerto Rico and Guam, broadening its reach across key areas.

While specific regional market share breakdowns aren't publicly detailed, MGIC's status as one of the largest private mortgage insurers indicates a broad presence. This reach encompasses various states and metropolitan areas, reflecting a significant footprint in the U.S. housing market.

MGIC's focus on private mortgage insurance inherently targets homebuyers. This includes those with lower down payments, suggesting a presence in areas with higher demand for affordable homeownership. This approach allows MGIC to serve diverse housing markets with varying price points and income levels, catering to a wide range of customer demographics.

Local Partnerships

MGIC localizes its offerings by directly engaging with lenders across these regions. This strategy ensures that the company remains accessible and responsive to the needs of its customers and partners.

Strategic Initiatives

The company's strategic initiatives center on executing business strategies and supporting customers with high-quality products. It also focuses on providing innovative solutions to meet the evolving needs of the mortgage market.

Market Leadership

MGIC's consistent performance and market leadership indicate a stable and widespread presence. This is further supported by its strong financial results and continued innovation in the mortgage insurance sector.

2024 Underwriting Performance

In 2024, MGIC was the top underwriter, with new insurance written (NIW) of $55.7 billion. This demonstrates its significant role in the private mortgage insurance market.

Overall Market Context

The private mortgage insurance market as a whole saw $298.9 billion in NIW in 2024. This places MGIC's performance within the broader industry context, highlighting its substantial contribution.

Customer Acquisition

MGIC's customer acquisition process is closely tied to its relationships with lenders. These partnerships are crucial for reaching the target market and providing mortgage insurance solutions. For more details on the company's growth strategy, see the Growth Strategy of MGIC.

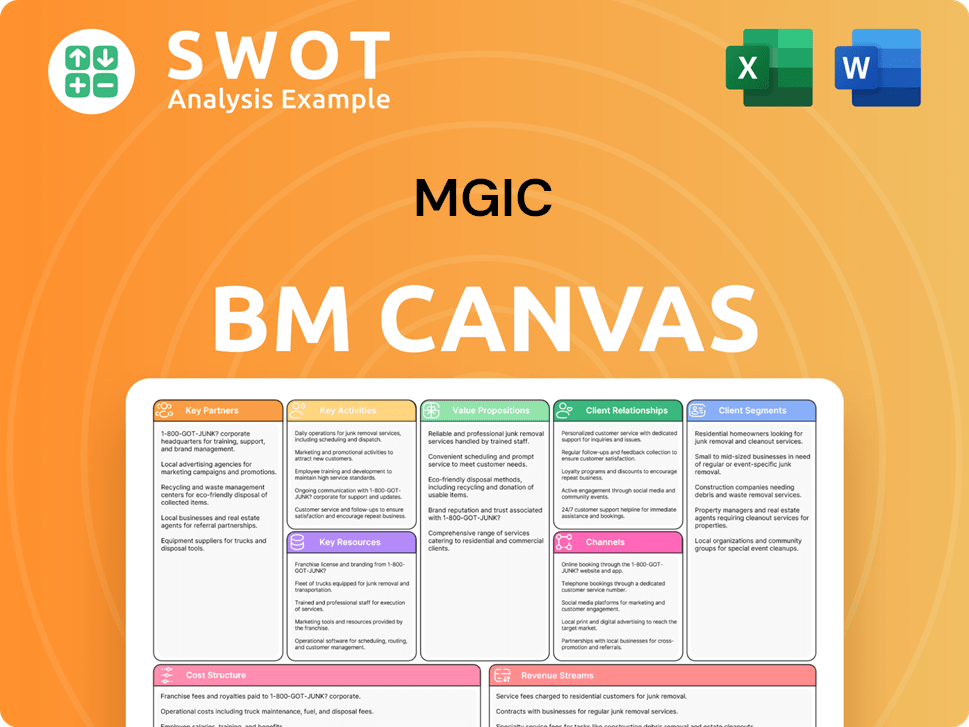

MGIC Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does MGIC Win & Keep Customers?

The customer acquisition and retention strategies of MGIC, a company focused on mortgage insurance, are primarily geared towards mortgage lenders and financial institutions. This business-to-business (B2B) approach requires a distinct strategy compared to businesses that directly serve consumers. MGIC's success hinges on attracting and retaining these key partners.

To acquire new customers, MGIC employs a multifaceted digital marketing approach. This includes targeted advertising campaigns on platforms like LinkedIn, specifically designed to reach financial professionals. Furthermore, the company uses Google Ads and programmatic display advertising to increase visibility and generate leads within the mortgage lending sector. The use of industry events also plays a role in building relationships.

Retention strategies are centered on providing significant value to lenders. This involves offering comprehensive underwriting services, leveraging advanced analytics and risk management tools to help lenders manage mortgage-related risks effectively. The company's commitment to innovation, such as developing digital mortgage insurance platforms and using AI for fraud detection, contributes to customer retention by enhancing the overall value proposition.

MGIC allocates approximately $2.4 million annually to digital marketing efforts. These efforts include LinkedIn sponsored content and targeted Google Ads. The company also utilizes programmatic display advertising to reach potential clients in the mortgage lending sector.

MGIC's Google Ads campaigns have a 3.2% click-through rate in the mortgage lending sector. Programmatic display advertising campaigns have a 0.6% conversion rate. MGIC focuses on providing high-quality products and innovative solutions to support its customers.

MGIC focuses on providing valuable products, services, and support to lenders. This includes offering underwriting and other services related to home mortgage lending. The company emphasizes leveraging analytics and risk management tools.

MGIC reported a full-year 2024 net income of $763 million and returned $700 million to shareholders through buybacks and dividends. This represents a 92% payout ratio, which can signal stability and reliability to its B2B clients. In April 2025, the company approved an additional $750 million share repurchase program.

Customer data and segmentation are essential for tailoring campaigns and offerings. The company aims to provide high-quality products and innovative solutions to support its customers. Successful retention is also linked to the company's strong financial performance and consistent capital returns to shareholders, which can signal stability and reliability. For a deeper understanding of MGIC's financial model, consider reading about the Revenue Streams & Business Model of MGIC.

MGIC's Target Market

MGIC's target market primarily consists of mortgage lenders and financial institutions. The company focuses on providing services that support these entities in their mortgage lending activities.

Customer Segmentation

MGIC uses data and segmentation to target campaigns and tailor its offerings. This allows the company to provide more relevant and effective services to its clients.

Impact of Economic Factors

The company expects persistency to remain high in 2025, supported by elevated mortgage rates. This is because the extended life of loans directly benefits mortgage insurance policies.

Financial Stability

MGIC's strong financial performance and consistent capital returns to shareholders signal stability and reliability to its B2B clients. This contributes to customer retention.

Innovation and Value Proposition

MGIC's commitment to innovation, such as developing digital mortgage insurance platforms and using AI for fraud detection, enhances the value proposition for its customers.

Customer Acquisition Process

The customer acquisition process involves digital marketing, industry events, and potentially referral platforms. The company targets financial professionals through various online channels.

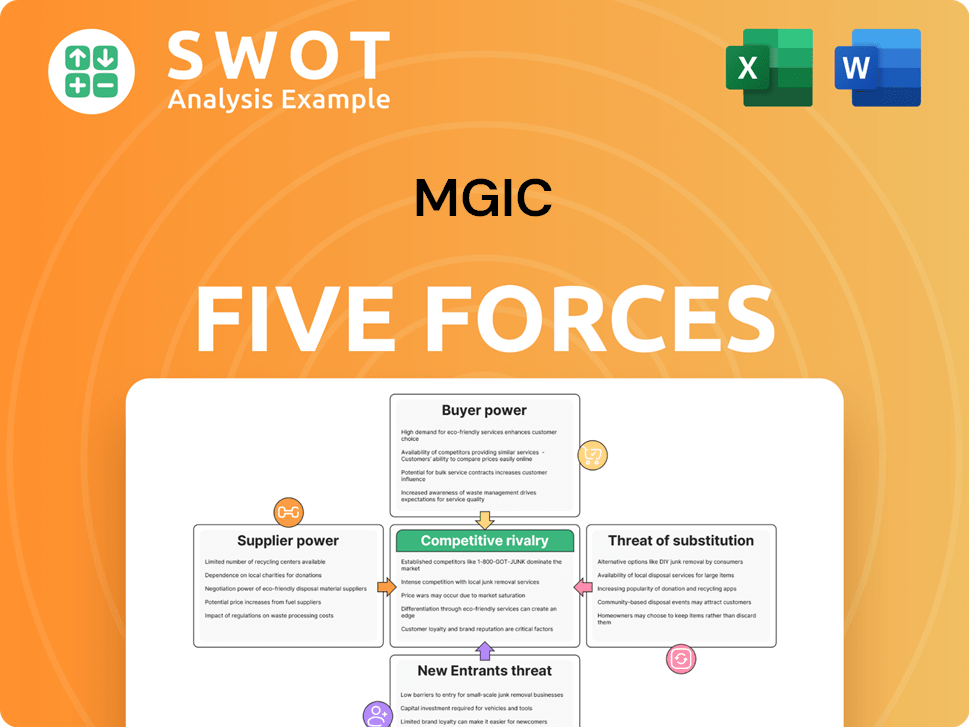

MGIC Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of MGIC Company?

- What is Competitive Landscape of MGIC Company?

- What is Growth Strategy and Future Prospects of MGIC Company?

- How Does MGIC Company Work?

- What is Sales and Marketing Strategy of MGIC Company?

- What is Brief History of MGIC Company?

- Who Owns MGIC Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.