MGIC Bundle

Can MGIC Continue to Dominate the Mortgage Insurance Landscape?

MGIC Investment Corporation, a cornerstone of the U.S. housing market since 1957, plays a pivotal role in enabling homeownership through private mortgage insurance. But what is the MGIC SWOT Analysis, and how does it plan to navigate the ever-changing financial terrain? This exploration dives deep into MGIC's strategic initiatives and financial projections.

Understanding MGIC's growth strategy is crucial for investors and industry professionals alike, especially considering the dynamic nature of the mortgage insurance sector. This analysis will dissect MGIC's future prospects, examining its market share, financial performance, and how it aims to capitalize on emerging opportunities. We'll also explore potential risks and the company's strategic responses to maintain its competitive edge in the mortgage insurance market.

How Is MGIC Expanding Its Reach?

The expansion initiatives of MGIC are primarily centered on reinforcing its leadership in the private mortgage insurance sector. This is achieved through disciplined underwriting and strategic capital management. The company's focus remains on its core business: insuring mortgage loans with low down payments. The strategic moves indicate a commitment to strengthening its existing market position, rather than venturing into new, unrelated areas.

A key aspect of MGIC's strategy involves maintaining a high-quality, well-balanced insurance portfolio. This is accomplished by adhering to strong underwriting standards. In the first quarter of 2025, MGIC wrote $10 billion in new insurance, while maintaining a new notice claim rate of 7.5%. This focus on quality and risk management is critical for sustainable growth. The company's approach also includes robust capital allocation, including substantial share repurchases and dividends.

MGIC's commitment to its core business and disciplined approach to expansion are key factors in its Marketing Strategy of MGIC. The company's focus on capital management and risk mitigation positions it well for future growth in the mortgage insurance market.

MGIC's capital allocation strategy is a significant part of its growth plan. The company has demonstrated confidence in its financial strength by returning capital to shareholders through share repurchases and dividends. This approach reflects a commitment to creating shareholder value.

MGIC utilizes reinsurance deals to enhance capital flexibility and risk absorption. These agreements provide additional protection against potential losses. This strategy helps the company manage its risk profile effectively. The $250.6 million reinsurance coverage on eligible new insurance written (NIW) from 2020, effective March 1, 2025, is an example of this approach.

In Q1 2025, MGIC repurchased 9.2 million shares for $224 million. This demonstrates the company's commitment to returning value to shareholders. An additional $65.8 million was repurchased through April 25, 2025.

A new $750 million share repurchase program was approved through 2027. This program underscores MGIC's confidence in its financial stability. This plan is designed to provide long-term value for shareholders.

Key Expansion Strategies

MGIC's growth strategy focuses on maintaining its leadership in the private mortgage insurance sector. The company prioritizes disciplined underwriting and strategic capital management. These strategies are designed to ensure long-term sustainability and profitability.

- Disciplined Underwriting: Maintaining high standards to manage risk and ensure portfolio quality.

- Strategic Capital Management: Utilizing share repurchases and dividends to return capital to shareholders.

- Reinsurance Agreements: Enhancing capital flexibility and risk absorption through strategic reinsurance deals.

- Focus on Core Business: Concentrating on insuring mortgage loans with low down payments.

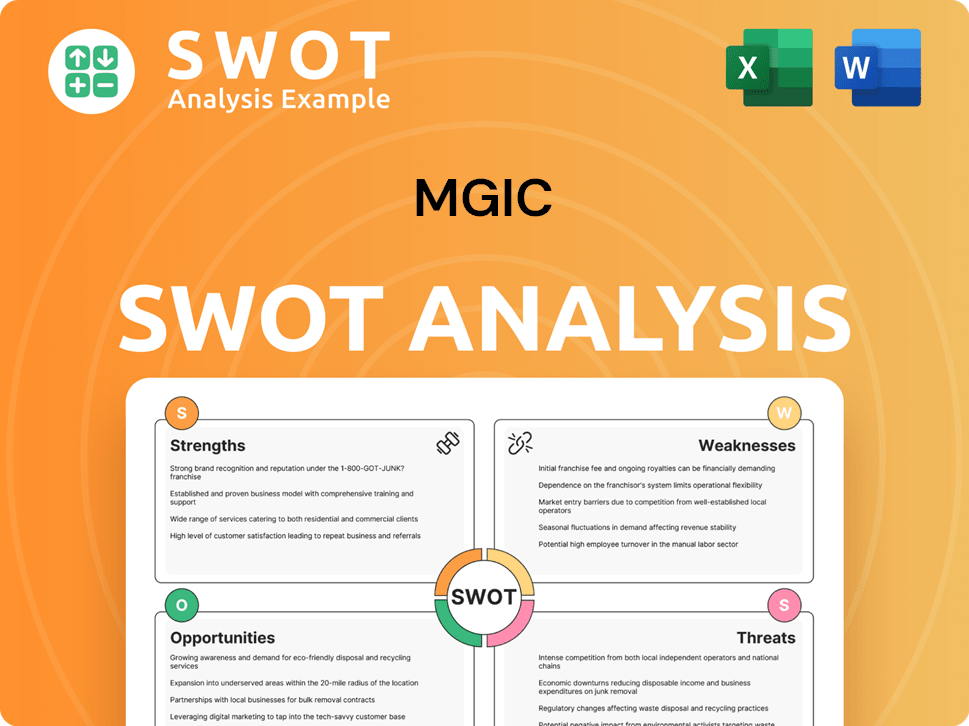

MGIC SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does MGIC Invest in Innovation?

The growth strategy of MGIC, a leading provider of mortgage insurance, is heavily influenced by its technological advancements. The company leverages technology to boost operational efficiency, enhance underwriting accuracy, and improve customer service. This approach is critical for maintaining its market position and navigating the complexities of the mortgage industry.

MGIC's commitment to 'high-quality products and innovative solutions' highlights its ongoing efforts to improve service offerings through technological means. This includes digital transformation initiatives aimed at streamlining processes for lenders and enhancing the overall customer experience. While specific details on large-scale R&D investments are not extensively publicized, the focus on prudent risk management and efficient operations implies continuous internal development and adoption of technologies.

The company's strategic use of technology is evident in its ability to maintain strong underwriting standards and effectively manage its insurance portfolio. This is supported by data-driven capabilities and sophisticated systems. The company's weighted average original FICO® of 746 and a weighted average original LTV of 93% for its insurance-in-force are indicators of this. This data-driven approach is essential for long-term growth.

Data Analytics and Underwriting

MGIC uses advanced data analytics to assess risk and make informed underwriting decisions. This helps maintain the quality of its insurance portfolio. The company's focus on data-driven insights is a key part of its strategy.

Digital Transformation

MGIC is likely involved in digital transformation initiatives to streamline processes for lenders. This includes online platforms and automated systems. These efforts improve efficiency and customer experience.

Risk Management

The company's focus on risk management is supported by internal systems and data analysis. This includes the use of sophisticated models. This helps in identifying and mitigating potential risks.

Customer Experience

MGIC aims to improve customer experience through technological means. This includes providing better online services and support. The goal is to make interactions easier and more efficient.

Operational Efficiency

Technology enhances operational efficiency by automating processes and reducing manual tasks. This leads to faster turnaround times and lower costs. MGIC's investments in technology support these goals.

Innovation in Products

MGIC continually seeks innovative solutions to meet the evolving needs of its customers. This might involve developing new insurance products or enhancing existing ones. The company's approach is customer-centric.

Impact of Technology on MGIC's Growth

Technology plays a crucial role in MGIC's growth strategy. It supports efficient operations, accurate underwriting, and improved customer service. The company's approach to innovation is integral to its success in the mortgage insurance market. For further insight into the company's values, consider reading about the Mission, Vision & Core Values of MGIC.

- Market Share: By using technology for better risk management and operational efficiency, MGIC aims to maintain or increase its market share in the competitive mortgage insurance industry.

- Financial Performance: Technology helps improve financial performance by reducing costs, improving underwriting accuracy, and enhancing customer satisfaction.

- Competitive Advantages: MGIC's investment in technology provides a competitive edge by enabling it to offer better services and manage risks more effectively than competitors.

- Future Prospects: The company's ability to adapt and integrate new technologies will be crucial for its future prospects, especially in a rapidly changing market environment.

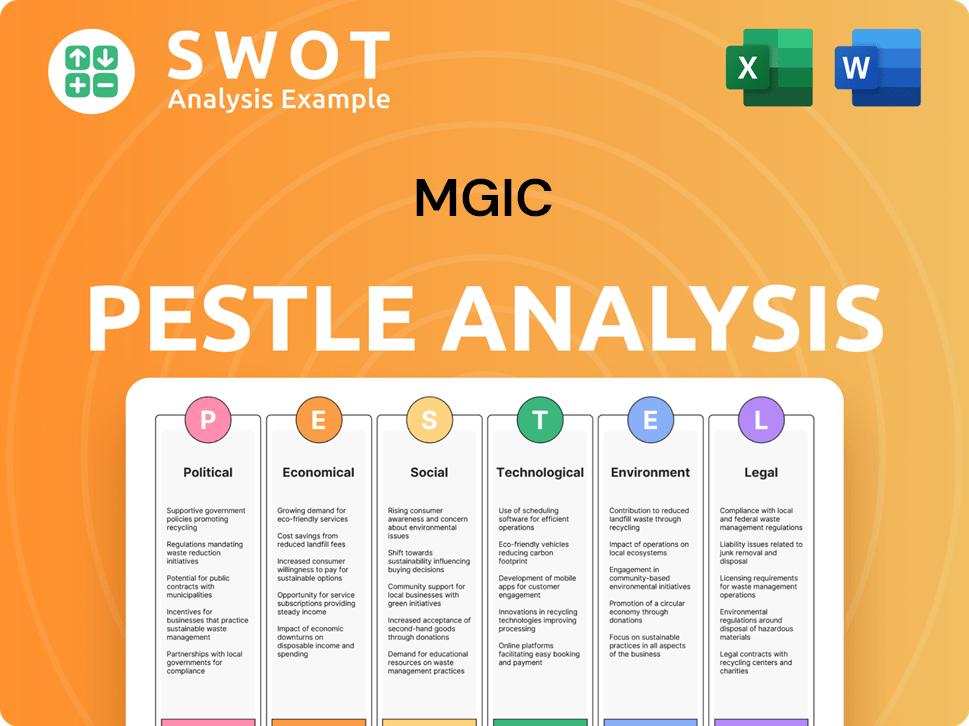

MGIC PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is MGIC’s Growth Forecast?

The financial outlook for MGIC Investment Corporation is positive, driven by strong earnings and strategic capital management. The company’s performance in the first quarter of 2025 reflects its ability to navigate market conditions effectively. This solid financial foundation supports a favorable view of MGIC's future prospects.

MGIC's Q1 2025 results demonstrate consistent financial health. The company’s focus on returning capital to shareholders through share repurchases and dividends further enhances its appeal. These actions, combined with a robust capital position, underscore MGIC's commitment to creating shareholder value and its strategic approach to growth.

In Q1 2025, MGIC reported a net income of $185.5 million, or $0.75 per diluted share. This is an increase from $174.1 million, or $0.64 per diluted share, in Q1 2024. Adjusted net operating income also rose to $0.75 per diluted share, up from $0.65 in the prior year. The company's annualized return on equity (ROE) for Q1 2025 was 14.3%.

Revenue for Q1 2025 was $306.23 million, with net premiums earned at $243.72 million. Net investment income remained steady at $61 million. The book yield on the investment portfolio was 3.8%.

MGIC repurchased $224 million of shares and paid $33 million in common stock dividends in Q1 2025. A new $750 million share repurchase program has been approved through 2027. The book value per share increased by 13% year-over-year to $21.40 as of March 31, 2025.

MGIC's PMIERs Available Assets totaled $5.9 billion, which is $2.6 billion above its Minimum Required Assets as of March 31, 2025, demonstrating robust liquidity and financial strength. Analysts have revised earnings estimates upward, reflecting confidence in MGIC's operational efficiency and market conditions.

MGIC's Growth Strategy and Future Prospects

MGIC’s future prospects are supported by its robust financial performance and strategic capital management. The company’s ability to generate strong earnings and return capital to shareholders positions it well for continued success. The company is focused on its MGIC growth strategy, including returning excess capital to shareholders through share repurchases and common stock dividends. MGIC's MGIC future prospects look promising, driven by its strong financial position and strategic initiatives.

- Mortgage insurance is a key sector for MGIC.

- The company's commitment to returning capital to shareholders.

- Analysts have revised earnings estimates upward, reflecting confidence in MGIC's operational efficiency and market conditions.

- MGIC's PMIERs Available Assets totaled $5.9 billion.

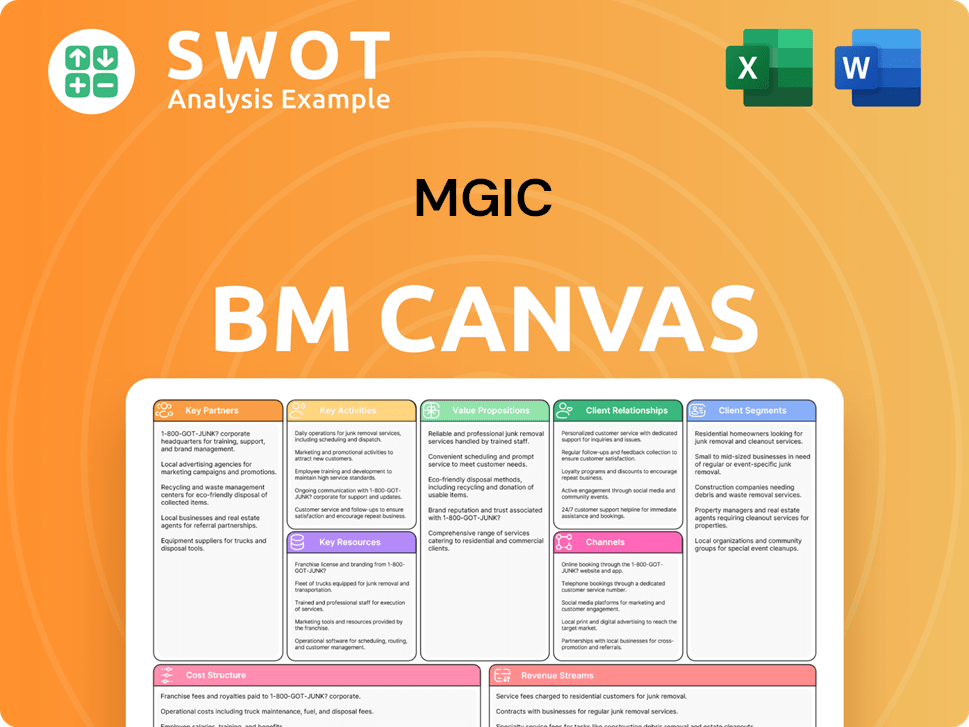

MGIC Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow MGIC’s Growth?

The success of MGIC's growth strategy and its future prospects are subject to several risks and obstacles. Housing affordability, a key factor influencing demand for low-down-payment mortgages, presents a significant challenge. Economic downturns and job market fluctuations could increase mortgage defaults, impacting MGIC's financial performance.

While MGIC maintains strong underwriting standards, evidenced by a large portion of its portfolio tied to high FICO scores, delinquency rates are a key metric to watch. The company faces market competition within the private mortgage insurance sector, which could affect its market share. Regulatory changes from the FHFA and modifications to GSE requirements also pose potential risks, influencing operational costs and strategies.

To mitigate these risks, MGIC employs a disciplined approach to risk and capital management. The company sets reserves to be sufficient across a wide range of outcomes, not just base-case scenarios. Diversification within its insurance portfolio and strategic reinsurance deals help strengthen risk absorption and enhance capital flexibility. For instance, a reinsurance transaction of $250.6 million was effective March 1, 2025.

Housing Affordability Concerns

Housing affordability directly impacts demand for low-down-payment mortgages, a core segment for MGIC. Decreased affordability can lead to reduced mortgage originations, affecting the company's revenue. This is a critical factor in evaluating MGIC's future prospects.

Economic Uncertainties

Economic downturns and softening job markets could increase mortgage defaults. This can lead to higher claims for MGIC, impacting profitability. Monitoring economic indicators is crucial for understanding the risks and opportunities for MGIC.

Market Competition

Competition in the private mortgage insurance sector poses a risk to MGIC's market share. Increased competition may lead to pricing pressures or reduced profitability. Understanding MGIC's competitive advantages in the mortgage insurance market is vital.

Regulatory Changes

Changes from the FHFA and GSE requirements can influence operational costs and strategies. These changes may strain capital reserves. MGIC's strategic initiatives for expansion must consider these regulatory impacts.

Delinquency Rates

Delinquency rates are a monitored metric that can indicate rising claims costs. While the primary delinquency inventory dipped from Q4 2024 to Q1 2025, it rose 5% year-over-year. The average reserve per delinquent loan increased.

Risk and Capital Management

MGIC's disciplined approach includes setting reserves for a wide range of outcomes and using diversification. Strategic reinsurance deals, such as the $250.6 million transaction effective March 1, 2025, enhance capital flexibility. For more information about MGIC, you can visit Owners & Shareholders of MGIC.

The primary risk factors include housing market volatility, economic downturns, and changes in interest rates. These factors can directly affect mortgage originations and claims. Managing these risks is essential for MGIC's financial performance.

MGIC employs robust underwriting standards and conservative risk management practices. Diversification within its insurance portfolio and strategic reinsurance agreements help to mitigate potential losses. Actively advocating for favorable legislation is also a key strategy.

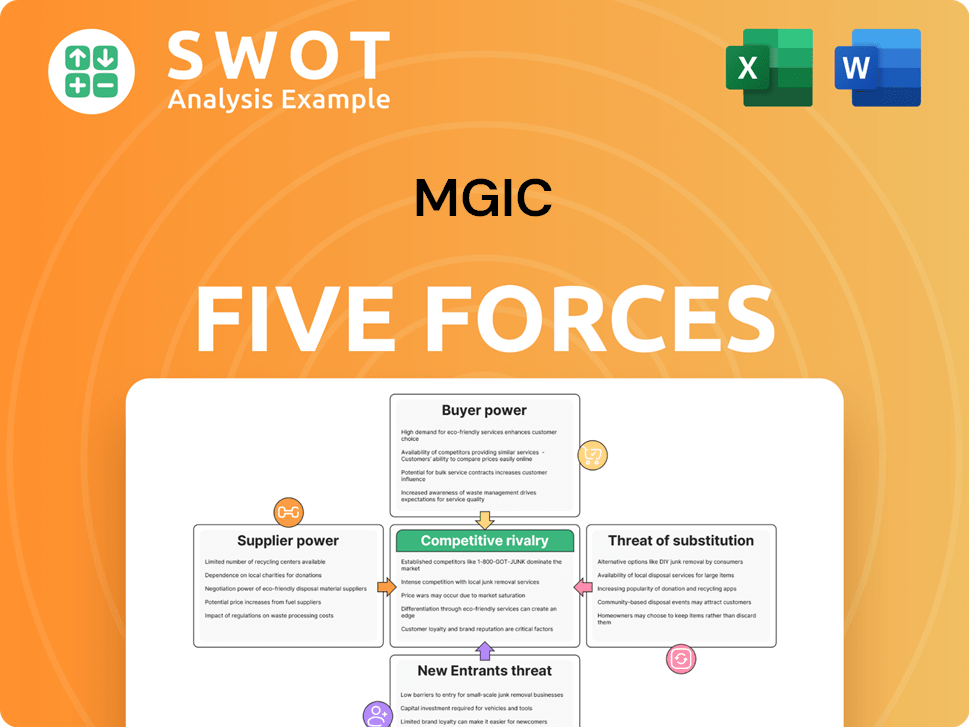

MGIC Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of MGIC Company?

- What is Competitive Landscape of MGIC Company?

- How Does MGIC Company Work?

- What is Sales and Marketing Strategy of MGIC Company?

- What is Brief History of MGIC Company?

- Who Owns MGIC Company?

- What is Customer Demographics and Target Market of MGIC Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.