Credito Real Bundle

What Went Wrong for Credito Real?

Delving into the Credito Real SWOT Analysis reveals the critical role of understanding customer demographics and target markets. For a financial institution like Credito Real, which catered to underserved segments, knowing its customer base was not just important, it was essential for survival. This analysis explores the company's journey, highlighting the impact of its target market on its ultimate fate.

This exploration of Credito Real’s customer demographics and target market offers a vital case study in market analysis within the financial services sector. By examining the company profile and its customer base, we can understand the challenges Credito Real faced. This analysis will uncover the intricacies of its customer acquisition strategy and the importance of adapting to changing market dynamics.

Who Are Credito Real’s Main Customers?

Understanding the customer demographics and target market of Crédito Real is crucial for analyzing its business model and strategic decisions. The company, a provider of financial services, primarily focused on underserved segments in Mexico and, later, expanded into other regions. This focus allowed Crédito Real to tap into significant market opportunities, particularly among low and middle-income individuals.

The primary customer base of Crédito Real consisted of individuals and small businesses. The company's approach to market analysis involved targeting those historically excluded from traditional financial institutions. This strategy was designed to capture a large portion of the population with specific income levels and geographic locations.

Crédito Real's customer profile typically included individuals with an average annual available income ranging from approximately $6,500 to $7,100 USD, often residing in suburban, urban, and rural areas. The company's market research indicated a strong presence in areas where access to financial services was limited. This approach helped Crédito Real establish a strong foothold in its target market.

Crédito Real served both consumers and small businesses (B2B). For consumers, the main products included payroll loans, microloans, and durable goods loans. The company's customer acquisition strategy also included SME loans, factoring, and leasing for working capital needs.

Payroll loans were a significant part of Crédito Real's portfolio, granted to Mexican unionized federal, state, and local public-sector employees, retirees, and pensioners. These loans, repaid through payroll deductions, mitigated default risk. By 2017, payroll and group loans represented 82% of Crédito Real's loan book.

Small and medium-sized enterprise (SME) loans, including credit loans, factoring, and leasing, were granted for working capital needs to businesses in Mexico and the US. While specific demographic breakdowns for SME customers are less detailed, the overall focus remained on underserved segments.

Crédito Real expanded its target market with its product diversification and geographic reach. Its entry into the US market with used car loans through Don Carro and the acquisition of AFS Acceptance in 2015 targeted the Hispanic segment without credit history, a demographic of close to 50 million people.

The company's customer segmentation strategies evolved over time to include a broader range of demographics. This expansion was part of a larger effort to capture new growth opportunities and meet the diverse needs of its target audience. For more details on the company's overall strategy, you can read about the Growth Strategy of Credito Real.

Key Customer Demographics

Crédito Real's target market primarily consisted of low and middle-income individuals in Mexico and the US. The company's focus was on providing financial services to those underserved by traditional institutions.

- Income Levels: Average annual available income of approximately $6,500 to $7,100 USD.

- Geographic Location: Suburban, urban, and rural areas in Mexico and the US.

- Customer Segments: Consumers (B2C) and small businesses (B2B).

- Product Focus: Payroll loans, microloans, durable goods loans, SME loans, factoring, and leasing.

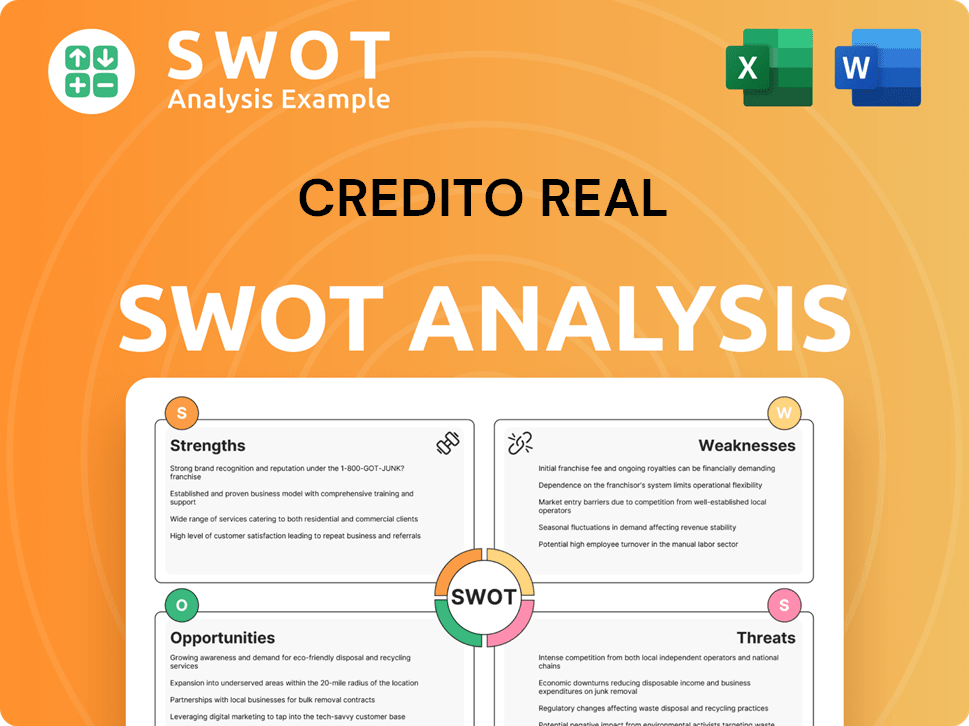

Credito Real SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Do Credito Real’s Customers Want?

Understanding the customer needs and preferences is crucial for any financial institution. For Crédito Real, this meant focusing on the underserved low and middle-income individuals and SMEs in Mexico. Their target market sought accessible financial services, a need often unmet by traditional banks, driving them to seek alternative credit solutions.

The core need was access to flexible credit products. Customers aimed to finance essential purchases, manage cash flow, or fund small business operations. The psychological aspect included aspirations for an improved quality of life and financial inclusion. This focus on providing financial services to those historically excluded shaped Crédito Real's approach.

The purchasing behaviors of Crédito Real's customers were heavily influenced by the accessibility and convenience of loan products. Payroll loans, with their direct salary deductions, offered streamlined repayment, reducing default risk. Financing 'white line goods' through retail partnerships addressed immediate household needs. This approach, coupled with a vast sales representative network, played a significant role in customer acquisition and credit access.

Key Customer Needs and Preferences

Crédito Real's customer base, primarily in Mexico, demonstrated specific needs and preferences. These included the need for accessible and flexible credit options, especially for those underserved by traditional banking. The company focused on providing solutions tailored to their target market's financial needs, such as payroll loans and financing for durable goods.

- Accessibility: Customers valued easy access to loans, with simplified application processes.

- Flexibility: The ability to choose from various loan products, like payroll, SME, and personal loans, was important.

- Convenience: Streamlined repayment methods, such as direct salary deductions, were highly preferred.

- Financial Inclusion: The opportunity to access financial services, particularly for those excluded by traditional banks, was a key driver.

Crédito Real addressed pain points like limited access to credit and stringent requirements from traditional banks. The company expanded its product offerings, including payroll, SME, and personal loans, to meet evolving market demands. Acquisitions like Instacredit and Don Carro demonstrated efforts to tailor offerings to specific regional and demographic preferences. Collaborations with fintech partners, such as ReSuelve and Credilikeme, further enhanced accessibility and banking operations. For more insights, explore the Revenue Streams & Business Model of Credito Real.

Credito Real PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Where does Credito Real operate?

The primary geographic focus of Crédito Real was Mexico, where it established itself as a leading financial institution. The company's operations extended across all 32 Mexican states. Beyond Mexico, Crédito Real expanded into the United States and Central America, specifically targeting countries like Costa Rica, Nicaragua, Panama, and Honduras. This strategic expansion allowed the company to diversify its market presence and reach a broader customer base.

In Mexico, Crédito Real aimed to serve the low and middle-income segments, which constituted a significant portion of the population. The company's distribution network in Mexico included over 10,000 sales representatives and strategic alliances with specialized operators. These partnerships enabled Crédito Real to effectively reach customers in various areas, including suburban, urban, and rural locations. The company's ability to localize its services was a key factor in its success in the Mexican market.

In the United States, Crédito Real's presence was primarily through its used car subprime lending subsidiary, Crédito Real USA Finance, LLC, which underwrote loans in 30 states. This subsidiary operated independently and collaborated with a network of over 1,500 auto dealers. The company's geographic distribution of sales reflected its diversified portfolio, with payroll loans, SMEs, personal loans, and used cars contributing to its total income.

Crédito Real's primary focus was the Mexican market, serving low and middle-income segments. It utilized a vast network of sales representatives and strategic alliances to reach customers across the country. This localized approach was crucial for effectively serving the target market within Mexico.

In the United States, Crédito Real operated through its subsidiary, Crédito Real USA Finance, LLC, focusing on used car subprime lending. This subsidiary served customers in 30 states, partnering with a network of auto dealers. The U.S. market expansion targeted specific segments within the Hispanic community.

Crédito Real expanded into Central America through the acquisition of Instacredit, a personal loans company. This acquisition provided a network of branches in Costa Rica, Nicaragua, and Panama. This expansion allowed access to stable markets with high-yield financial products.

Strategic decisions included selling Crédito Real USA Finance LLC and a portion of its SME loan portfolio. These moves aimed to refocus on core activities and improve the non-performing loan profile. These strategic shifts were part of a broader effort to optimize the company's financial performance.

Key Geographic Markets

Crédito Real's geographic strategy focused on key markets to serve its customer demographics.

- Mexico: Strong presence across all 32 states, targeting low and middle-income segments.

- United States: Used car subprime lending in 30 states, focusing on specific demographic groups.

- Central America: Expansion through Instacredit, with branches in Costa Rica, Nicaragua, and Panama.

- Strategic Adjustments: Sales of subsidiaries and loan portfolios to refocus on core activities.

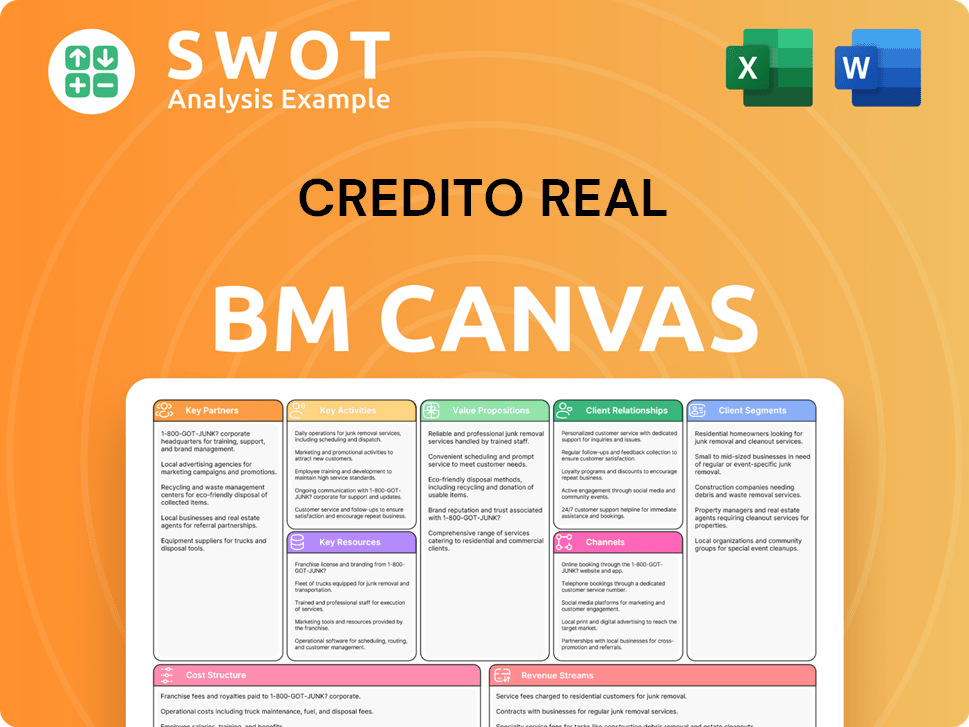

Credito Real Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Does Credito Real Win & Keep Customers?

The customer acquisition and retention strategies employed by Crédito Real centered on a robust distribution network and strategic alliances, particularly within Mexico. Their approach focused on directly serving low and middle-income segments, a key aspect of their customer demographics. This strategy, combined with a diversified product platform, aimed to meet the specific financial needs of their target market.

Crédito Real's extensive on-site presence, with over 10,000 sales representatives, was pivotal in reaching their target audience. They formed strategic partnerships, including equity stakes in distributors like Kondinero, which provided exclusive access to unionized public-sector employees and pensioners. These alliances were crucial for origination and expanding their reach.

The company's sales tactics involved providing financial services to underserved populations, often overlooked by traditional financial institutions. Their product range included payroll loans, durable goods loans, and small business loans, tailored to the needs of specific customer groups. For example, used car loans targeted the Hispanic population in the US without Social Security numbers.

Crédito Real utilized a vast network of over 10,000 sales representatives and strategic alliances to acquire customers. Key partnerships, such as with Kondinero, provided exclusive access to specific customer segments. These relationships were essential for efficient origination and reaching their target market.

The company offered a diverse range of financial products, including payroll loans, durable goods loans, and small business loans. This diversification allowed Crédito Real to meet the varied financial needs of their customer demographics. Used car loans, for instance, targeted specific segments like the Hispanic population.

Crédito Real focused on low and middle-income segments, a key aspect of their target market. They tailored their products to meet the needs of these underserved groups, which differentiated them from traditional banks. This focus helped Crédito Real understand and serve its customer base.

While specific loyalty programs weren't extensively documented, Crédito Real demonstrated a commitment to building lasting relationships. Offering additional funds to borrowers before loan maturity suggests a retention strategy. Furthermore, their engagement with fintech points to enhancing customer experience.

Over time, Crédito Real expanded its operations, including acquisitions like Instacredit and Don Carro, which demonstrated strategic growth. Despite these efforts, the company faced significant challenges, leading to its liquidation in February 2022. This underscores the complexities of maintaining customer loyalty and managing risk, as highlighted in the Competitors Landscape of Credito Real.

Strategic Partnerships

Crédito Real's partnerships, particularly with distributors, were crucial for reaching its target market. These alliances provided exclusive origination channels and access to specific customer segments, enhancing their market penetration. These partnerships were key to their growth strategy.

Market Expansion

The acquisition of companies like Instacredit and Don Carro marked strategic expansions into new geographic markets. These moves aimed to diversify their portfolio and reach new customer segments. This expansion was a key part of their growth initiatives.

Digital Initiatives

Crédito Real collaborated with fintech partners to enhance financial access and improve customer experience. This move towards digital solutions aimed to streamline processes and increase customer engagement. This shows their adaptability to the fintech revolution.

Customer Focus

Crédito Real's long-term focus on understanding customer credit profiles indicated a strategy of building lasting relationships. This customer-centric approach was designed to foster repeat business and ensure customer satisfaction. This strategy was vital for their success.

Risk Management

The eventual liquidation of Crédito Real highlighted the importance of effective risk management. Despite successful acquisition strategies, the company faced challenges in maintaining customer loyalty and managing asset quality. This underscores the importance of risk assessment.

Market Segmentation

Crédito Real's focus on low and middle-income segments allowed them to tailor their products. This targeted approach helped them meet the specific needs of underserved populations. This strategy was crucial for their market positioning.

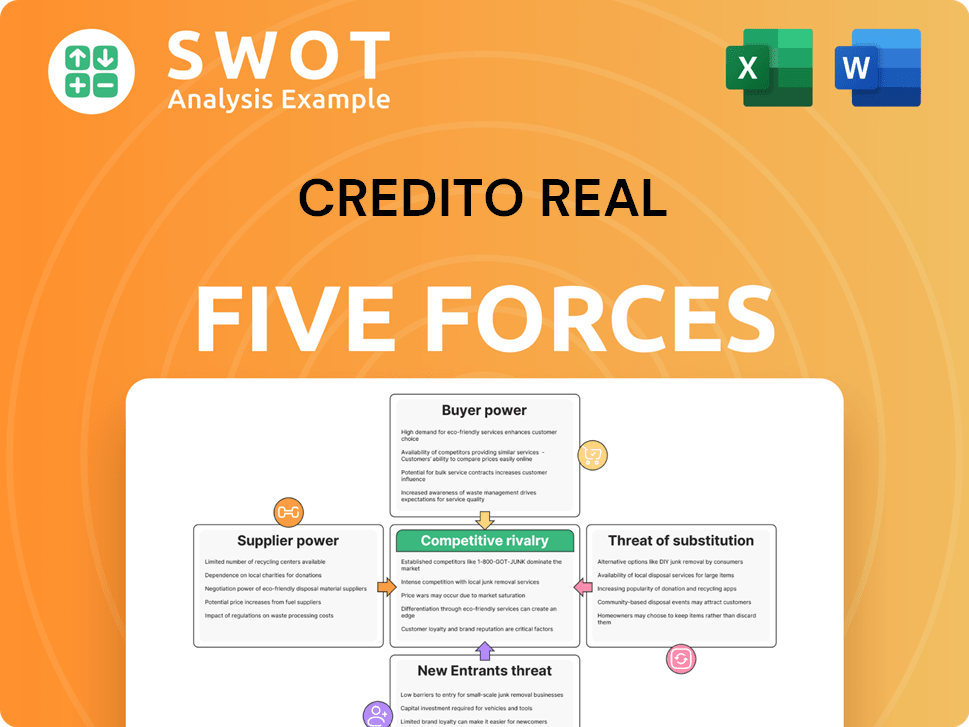

Credito Real Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Credito Real Company?

- What is Competitive Landscape of Credito Real Company?

- What is Growth Strategy and Future Prospects of Credito Real Company?

- How Does Credito Real Company Work?

- What is Sales and Marketing Strategy of Credito Real Company?

- What is Brief History of Credito Real Company?

- Who Owns Credito Real Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.