Credito Real Bundle

Can the Rise and Fall of Crédito Real Offer Lessons for Investors?

Crédito Real, a once-dominant player in Mexico's Credito Real SWOT Analysis financial services sector, presents a compelling case study in strategic growth and its potential pitfalls. Founded with the mission of financial inclusion, Crédito Real's journey from a small NBFI to a major lender is a story of ambition and challenges. This analysis explores the company's evolution, examining its growth strategy and the factors that ultimately shaped its future.

This deep dive into Crédito Real's Growth Strategy and Future Prospects examines the crucial decisions that propelled its expansion, the innovative approaches it adopted, and the financial realities that led to its current state. Understanding the Company Analysis of Crédito Real offers valuable insights for investors and business strategists, offering lessons on risk management and the impact of economic conditions on financial institutions. The analysis also provides a look at the Credito Real company financial performance and its Credito Real business model.

How Is Credito Real Expanding Its Reach?

Prior to its liquidation, the company, focused on expanding its reach and diversifying its financial product offerings. The core of its strategy involved providing financial solutions to segments often overlooked by traditional financial institutions. This included offering payroll loans to government and unionized employees, and microloans to small businesses, aiming to capture a significant portion of the market share.

The expansion initiatives included a national network of distributors to facilitate these loans. This distribution network was crucial for reaching the target customer base and efficiently delivering financial products. The company's growth strategy was heavily reliant on this network to drive loan origination and market penetration, especially in the areas where traditional banking services were less accessible.

Beyond Mexico, the company had international operations. This included a presence in Central America through its subsidiary, Instacredit. Instacredit offered various financial products such as consumer loans, SME loans, used vehicle loans, and home loans. Additionally, the company had interests in the US market through entities like Crédito Real USA Finance LLC and Crédito Real USA Business Capital, LLC. These international initiatives were designed to access new customer bases and diversify revenue streams. To learn more about the company's past, you can read a Brief History of Credito Real.

Instacredit, a subsidiary, operated in Central America. It offered consumer loans, SME loans, used vehicle loans, and home loans. This expansion aimed to diversify the company's revenue streams and customer base beyond Mexico.

The company had a presence in the US market through entities like Crédito Real USA Finance LLC and Crédito Real USA Business Capital, LLC. These entities were designed to capture a share of the US financial services market.

As part of its restructuring, the company began divesting non-core portfolios and assets. This included US assets and operations in Costa Rica. The restructuring involved transferring assets to a Mexican trust for administration and sale.

The restructuring aimed to streamline operations and focus on the core business. The goal was to improve financial stability and maximize returns for creditors. This strategic shift was crucial for addressing the company's financial challenges.

Key Expansion Strategies

The company's expansion strategy focused on reaching underserved markets and diversifying its financial products. This involved leveraging a national distribution network and expanding internationally.

- Payroll Loans: Targeting government and unionized employees.

- Microloans: Providing financial support to small businesses.

- International Operations: Expanding into Central America and the US.

- Divestiture: Streamlining operations by selling non-core assets.

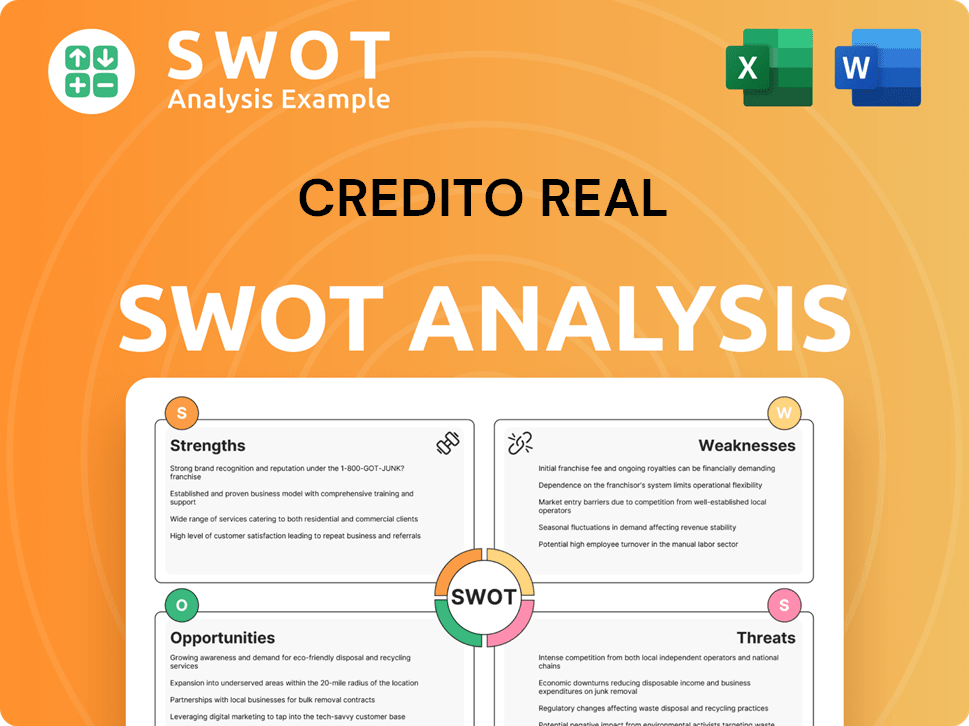

Credito Real SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Credito Real Invest in Innovation?

In its operational history, like many financial institutions, Crédito Real would have sought to leverage technology and innovation to enhance its services and reach. The financial landscape in Mexico has been rapidly evolving, with a strong emphasis on digital transformation and the adoption of fintech solutions.

As of 2024, the Mexican fintech sector experienced significant growth, with the number of companies founded by Mexican nationals increasing by almost 19% compared to 2023, reaching 773 companies. This indicates a dynamic environment where financial institutions, including non-banking financial institutions (NBFIs), needed to adopt digital solutions for customer acquisition, loan processing, and risk management to stay competitive.

The general trend in the financial industry, including in Mexico, points towards increased adoption of digital platforms, automation, and data analytics to streamline operations and improve customer experience. However, for Crédito Real, the focus has shifted from growth-oriented innovation to the technological infrastructure required for its liquidation process, including the management and monetization of its remaining assets through a trust.

Digital Transformation

The Mexican financial sector has seen a surge in digital platforms and automation. This shift is driven by the need to streamline operations and improve customer experience.

Fintech Growth

The Mexican fintech market is expanding rapidly. The number of fintech companies founded by Mexican nationals grew significantly in 2024.

Data Center Demand

There is a rising demand for data center capacity and infrastructure in the Mexican financial system. This indicates a push towards more robust technological foundations.

Liquidation Focus

For Crédito Real, the focus has shifted to managing the technological aspects of its liquidation. This includes handling and monetizing remaining assets.

Technological Infrastructure

The Mexican financial system is projected to require over $2 trillion in data center infrastructure over the next five years. This highlights the importance of technological foundations.

Competitive Advantage

Financial institutions need to adopt digital solutions to stay competitive. This includes customer acquisition, loan processing, and risk management.

The Mexican financial system has seen a rising demand for data center capacity and associated infrastructure, estimated to require over $2 trillion over the next five years, indicating a push towards more robust technological foundations. The shift towards digital platforms and automation is a key trend in the financial industry, including in Mexico. For a detailed overview of the company, further insights can be found in an article about the Credito Real by [insert link here] which offers a comprehensive company analysis.

Key Technological Strategies

Financial institutions are increasingly adopting digital platforms and automation. This includes using data analytics to improve customer experience and streamline operations.

- Digital Platforms: Implementing online and mobile platforms for customer interactions.

- Automation: Automating loan processing and other operational tasks.

- Data Analytics: Using data to improve risk management and customer service.

- Infrastructure: Investing in robust data center infrastructure to support digital operations.

Credito Real PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Credito Real’s Growth Forecast?

The financial outlook for Crédito Real is heavily influenced by its ongoing liquidation process. The company's situation has been significantly impacted by severe liquidity issues and defaults on bond payments. This led to a 'concurso mercantil' filing in Mexico in October 2023, a court-supervised restructuring. A restructuring plan was approved by creditors holding a majority of unsecured claims and subsequently by the Mexican court.

This restructuring plan, which became effective on March 28, 2025, involves transferring all remaining assets to a wind-down trust. The purpose of the trust is to liquidate the assets and distribute the proceeds to creditors. The entire process is designed to manage the financial fallout and provide a framework for creditor recovery.

As of June 2024, the estimated total unsecured claims against Crédito Real amounted to US$1.922 billion. The potential distributive value to unsecured creditors is estimated at US$382 million, representing an estimated recovery of 19.875%. The payout period is tentatively estimated at three years. The recognition of the Mexican insolvency proceedings by the U.S. Bankruptcy Court for the District of Delaware on March 11, 2025, under Chapter 15 of the U.S. Bankruptcy Code, was a crucial step.

Liquidation and Asset Transfer

Crédito Real's assets are being transferred to a wind-down trust. This trust is responsible for liquidating the assets and distributing the proceeds to creditors. This process is central to the restructuring plan approved by the Mexican court.

Unsecured Claims and Recovery

Total unsecured claims were estimated at US$1.922 billion as of June 2024. The estimated recovery for unsecured creditors is 19.875%, with a potential payout of US$382 million. The recovery is a key focus of the restructuring.

Timeline and Payout Period

The payout period for creditors is tentatively estimated at three years. This timeframe is crucial for the distribution of funds. The restructuring plan provides a structured timeline for creditor payments.

Chapter 15 Recognition

The U.S. Bankruptcy Court's recognition of the Mexican insolvency proceedings under Chapter 15 is significant. This allows for the cancellation of bank loans and unsecured notes. Creditors receive beneficial ownership interests in the Trust.

Impact on Creditors

Recognized creditors will receive beneficial ownership interests in the Trust. This mechanism is the primary means of recovery. The restructuring plan aims to provide a fair distribution of assets.

Future Investment Opportunities

Given the current liquidation, future investment opportunities are limited. The focus is on the recovery process and the distribution of assets. For more details, you can explore the Marketing Strategy of Credito Real.

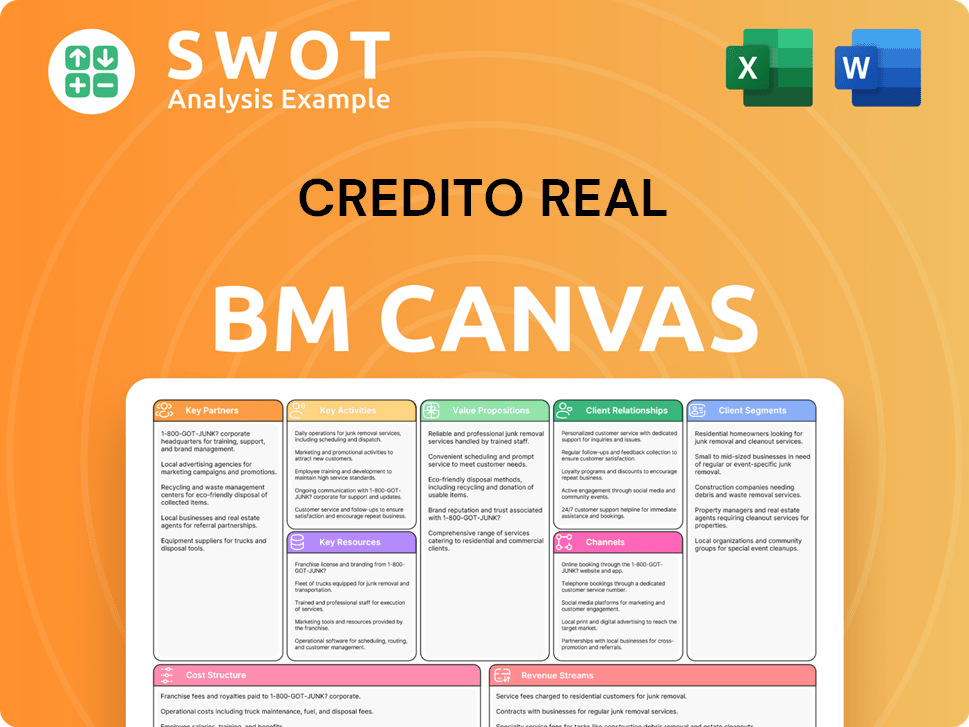

Credito Real Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Credito Real’s Growth?

The downfall of Crédito Real highlights significant risks and obstacles that can plague a financial services company. These issues, including liquidity problems and accounting irregularities, led to its liquidation. Analyzing these challenges offers valuable insights into the potential pitfalls of financial institutions and the importance of robust risk management.

Crédito Real's restructuring process, though intended to resolve its financial difficulties, has faced legal and operational hurdles. The complexities of cross-border insolvency proceedings and the potential for disputes among creditors underscore the intricate nature of such processes. Understanding these challenges is crucial for investors and stakeholders assessing the company's future.

The company's primary obstacle was severe liquidity constraints, worsened by the COVID-19 pandemic, leading to defaults on bond payments. Flawed accounting practices regarding loan book valuation also played a significant role, causing rating agencies to withdraw their credit ratings. These factors combined to create an unsustainable situation for Crédito Real.

Liquidity Constraints

Severe liquidity issues were a major factor in Crédito Real's downfall, directly impacting its ability to meet financial obligations. The inability to manage cash flow effectively ultimately led to defaults on bond payments. This highlights the critical importance of maintaining sufficient liquid assets within the Revenue Streams & Business Model of Credito Real.

Accounting Irregularities

Flawed accounting practices, particularly in the valuation of the loan book, misled auditors and led to the withdrawal of credit ratings. Such issues eroded investor confidence and contributed to the company's financial instability. Accurate and transparent financial reporting is vital for any financial services company.

Legal and Operational Challenges

The restructuring process presented legal and operational hurdles, including challenges to the bankruptcy proceedings. These complexities can significantly delay asset monetization and creditor payouts. Navigating these challenges requires careful legal and strategic planning.

Market Pressures

External market pressures, such as economic downturns, can severely impact a company's financial health. The company's ability to withstand such pressures is crucial for long-term survival. Understanding the impact of economic conditions is vital for assessing the company's future prospects.

Cross-Border Insolvency

Crédito Real's cross-border insolvency proceedings highlight the complexities of international financial restructuring. These processes often involve multiple jurisdictions and legal frameworks, which can lead to delays and increased costs. Understanding these intricate legal aspects is crucial.

Asset Monetization

The future trajectory of Crédito Real depends on the successful monetization of its assets. This involves selling off the remaining assets within the established trust and distributing the proceeds to creditors. The efficiency of this process will determine the final outcome for stakeholders.

In March 2025, the U.S. International Development Finance Corp. (DFC) appealed the U.S. recognition of Crédito Real's bankruptcy proceedings. The Mexican court approved the company's exit from bankruptcy in August 2024. These dates highlight the timeline of events and the ongoing legal challenges.

The legal challenges and cross-border insolvency issues have added complexity to the restructuring process. These difficulties can potentially impact the distribution of assets. The involvement of multiple jurisdictions and legal frameworks increases the complexity.

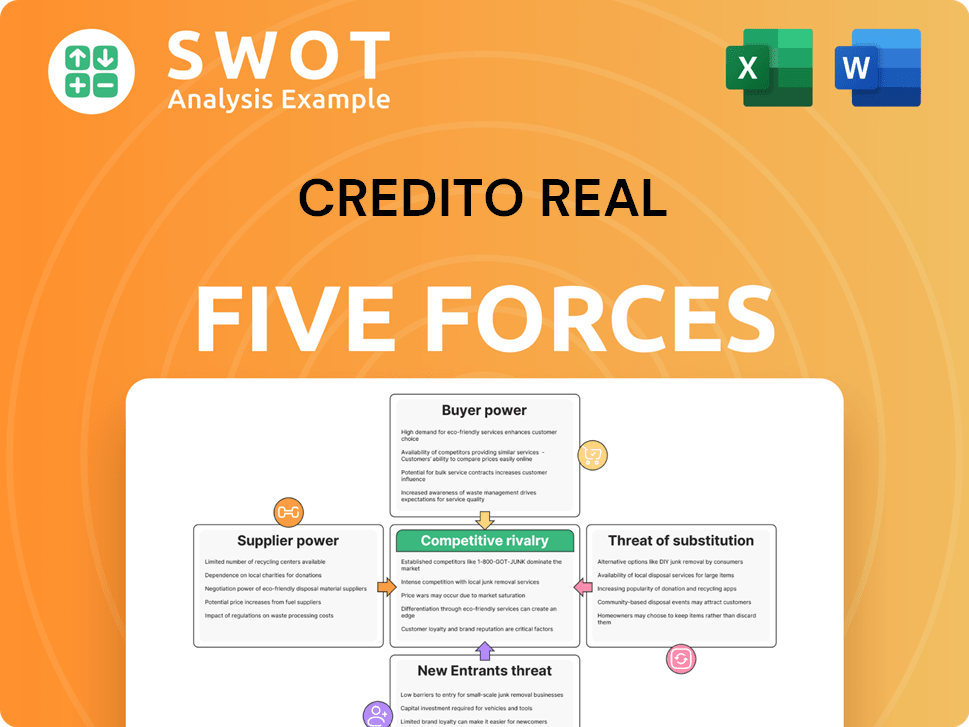

Credito Real Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Credito Real Company?

- What is Competitive Landscape of Credito Real Company?

- How Does Credito Real Company Work?

- What is Sales and Marketing Strategy of Credito Real Company?

- What is Brief History of Credito Real Company?

- Who Owns Credito Real Company?

- What is Customer Demographics and Target Market of Credito Real Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.