Small World Bundle

What Happened to Small World Financial Services?

Small World Financial Services, a once-dominant force in the global Small World SWOT Analysis money transfer landscape, has recently faced a dramatic operational shift. Founded in 2005, the company provided essential international money transfer services for individuals and businesses worldwide. However, its operations abruptly ceased in June 2024, leaving customers and retailers in a state of uncertainty.

This unexpected closure of Small World financial services highlights the inherent risks within the competitive money transfer services sector. The international money transfer market, including online money transfer, is experiencing rapid technological evolution and intense competition, with digital financial services growing significantly. Understanding the operational dynamics of Small World Company, its revenue models, and the factors contributing to its challenges is crucial for anyone involved in the financial services industry.

What Are the Key Operations Driving Small World’s Success?

Historically, Small World financial services focused on facilitating cross-border money transfers for individuals and small to medium-sized enterprises (SMEs). Their core services included various options for sending and receiving money, such as bank deposits, cash pickups, and mobile wallet top-ups. This enabled them to serve a diverse customer base, including individuals sending money internationally and SMEs needing international payment solutions.

The company’s approach combined physical branches, an extensive agent network, and online platforms. This hybrid model allowed them to reach a broad audience, including those in underserved markets. The digital aspect, with online and mobile platforms, increased convenience and accessibility, which was crucial for their operations.

The company’s supply chain relied heavily on partnerships with banking and payment networks. These partnerships were vital for expanding its distribution network and leveraging established financial infrastructure. These collaborations reportedly drove a 15% increase in transaction volume in 2024.

The core offerings of included a variety of options for sending and receiving money. These included bank deposits, cash pickups, and mobile wallet top-ups, catering to different customer preferences and needs. This variety helped to serve a broad customer base.

utilized a hybrid operational model that combined physical branches, a vast network of agents, and online platforms. As of Q1 2024, the company had over 200 branches and partnered with more than 100,000 agents globally. This model allowed for a widespread presence.

The core capabilities of translated into customer benefits by offering secure, fast, and affordable transfers. The goal was to avoid expensive bank fees and foreign currency exchange fees, providing a cost-effective solution. The in-house processing streamlined the delivery of funds.

The company's supply chain relied heavily on strategic alliances with banking and payment network partners. These partnerships were vital for expanding its distribution network and leveraging established financial infrastructure. These collaborations reportedly drove a 15% increase in transaction volume in 2024.

Value Proposition

offered secure, fast, and affordable money transfers, aiming to avoid high bank fees and currency exchange costs. This value proposition was particularly attractive to customers seeking cost-effective international money transfer services. The company's focus on customer convenience and cost savings set it apart.

- Secure and reliable money transfers.

- Competitive exchange rates.

- Multiple payout options, including bank deposits and mobile wallets.

- Extensive global network for wide accessibility.

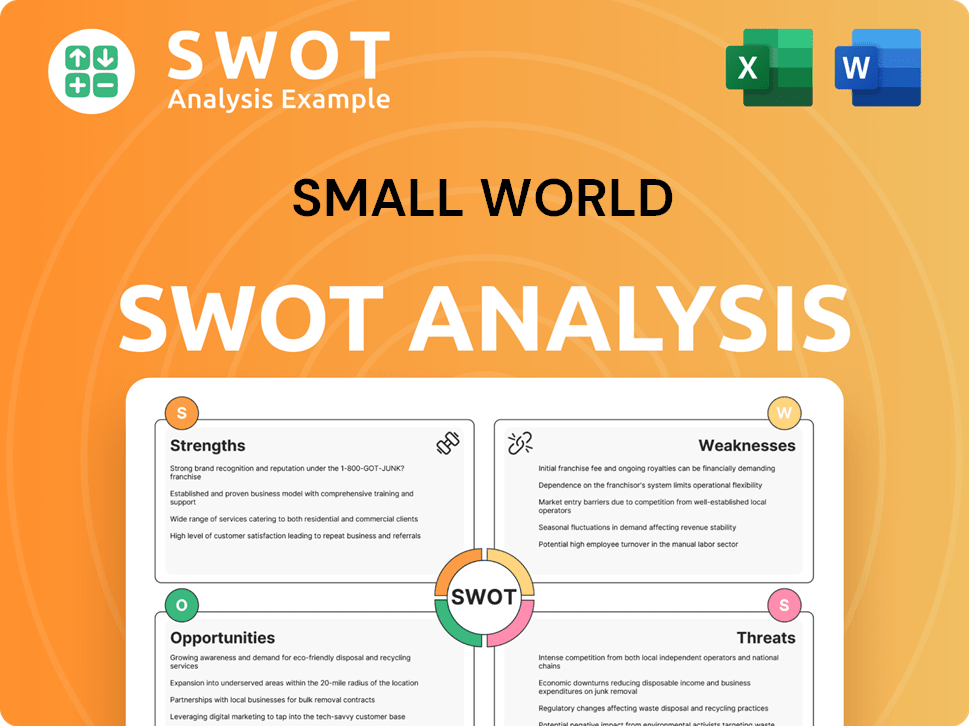

Small World SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Small World Make Money?

The primary revenue stream for Small World financial services was generated through fees applied to each money transfer transaction. The fee structure varied based on the specific service used, such as home or office delivery, where commissions were paid to delivery agents from the fees collected.

While precise recent financial data for Small World Company for 2024-2025 is unavailable, the 2022 accounts showed a processed volume of £5.2 billion and a revenue of £137 million. This indicates the scale of operations and the importance of fees in their business model.

In the competitive landscape of money transfer services, aggressive pricing is prevalent, leading to lower fees and rates. The industry saw an average commission rate drop of 15% in 2024 due to intense competition, putting pressure on companies like Small World money transfer to maintain profitability.

Industry Dynamics and Monetization Strategies

The money transfer agencies market was valued at an estimated $29.08 billion in 2024 and is projected to reach $48.81 billion by 2028, with a compound annual growth rate (CAGR) of 13.8%. This growth is fueled by increasing remittances, the adoption of digital wallets, and investments in technology infrastructure.

- Innovative monetization strategies include platform fees, bundled services, tiered pricing, and cross-selling.

- Small World Company's approach involves offering a wide array of payment options, from bank deposits to mobile wallets, catering to diverse customer needs.

- The company's integration with banks and mobile wallets, along with strategic partnerships, aims to broaden accessibility and enhance its global presence, which could indirectly support revenue growth.

- For more detailed insights into the company's growth strategy, you can refer to Growth Strategy of Small World.

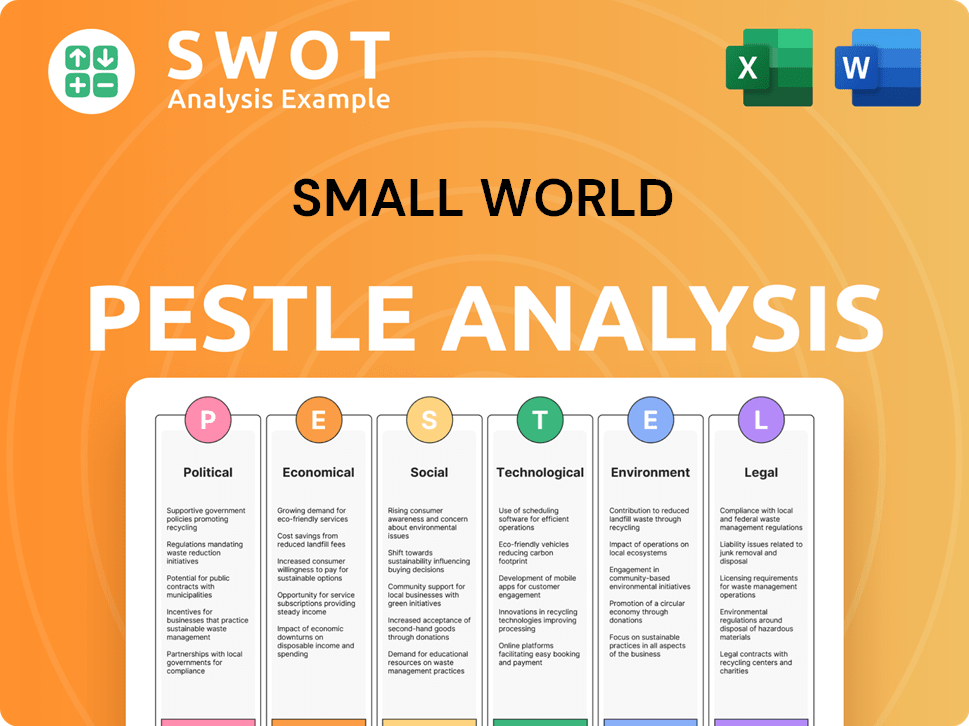

Small World PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped Small World’s Business Model?

The journey of Small World Financial Services, a key player in the money transfer services sector, was marked by significant growth and strategic maneuvers. Founded in 2005, the company expanded its reach through both organic growth and strategic acquisitions. This approach allowed it to build a substantial global network, which was a crucial part of its business model.

A pivotal moment was the merger with Choice Money Transfer in 2010, which significantly broadened its footprint across Europe and North America. This strategic move resulted in a combined turnover exceeding $2.5 billion. The company also invested in technology to streamline operations. However, despite its initial successes, the company faced substantial challenges that ultimately led to its downfall.

Small World Financial Services, despite its initial success, faced significant operational and market challenges. In June 2024, the company entered special administration, ceasing all services due to financial difficulties and regulatory issues. This abrupt closure affected thousands of customers, highlighting the volatile nature of the international money transfer market.

Small World Financial Services was established in 2005. It expanded through acquisitions, including Choice, Express Funds, and others. The merger with Choice Money Transfer in 2010 was a key strategic move. By Q1 2024, the company had over 200 branches and more than 100,000 agents worldwide.

The merger with Choice Money Transfer significantly expanded its presence. Investments in technology, such as Google Apps, were made to improve communication. Increased pricing in its final month of operation was an attempt to raise short-term funds. The company leveraged strategic partnerships with banks and mobile wallet services to expand its distribution network, which drove a 15% increase in transaction volume in 2024.

Small World Financial Services offered a broad global network and diverse payout options. It focused on secure, fast, and affordable transfers. The company aimed to differentiate itself from competitors like Western Union and MoneyGram. Strategic partnerships with banks and mobile wallet services were key to its expansion. The company was projected to boost market share by 10% by the end of 2025.

The company faced fines for competition breaches and rising compliance costs. Compliance costs rose by an average of 15% for financial institutions in 2024. A review of 2022 accounts showed warning signs. The company entered special administration in June 2024, ceasing all services. The financial difficulties and regulatory issues led to its ultimate closure.

Detailed Analysis

Small World Financial Services initially aimed to provide competitive money transfer services. It focused on a customer-centric approach. However, the company's failure highlights the intense competition and regulatory pressures within the industry. For a deeper understanding of the competitive landscape, you can review the Competitors Landscape of Small World.

- The company's global network included over 100,000 agents.

- The merger with Choice Money Transfer was a significant strategic move.

- Rising compliance costs and regulatory issues were key factors in its downfall.

- The company's abrupt closure impacted thousands of customers.

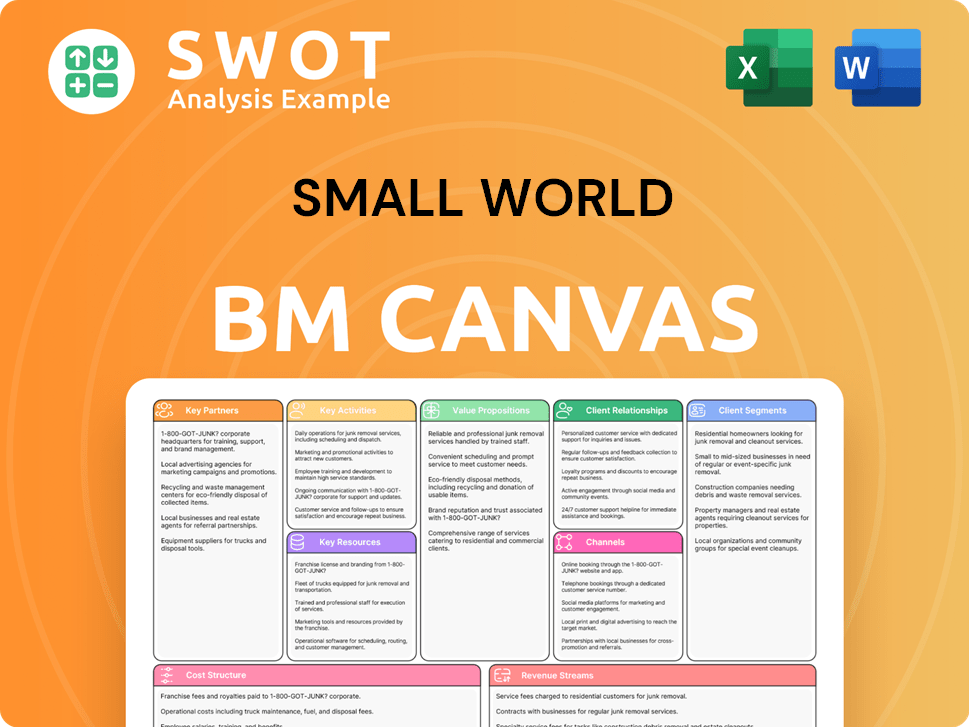

Small World Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is Small World Positioning Itself for Continued Success?

The Small World financial services once held a significant position in the global money transfer market, boasting a wide network. However, the company faced intense competition from major players like Western Union and digital fintech firms. In 2024, the digital financial services sector saw a 15% growth, intensifying rivalry and putting pressure on commission rates, which dropped by 15%.

Small World's market share in the digital remittance market was estimated at 0.6% in 2023. The company faced regulatory challenges, financial difficulties, and stiff competition, which significantly impacted its operations. These factors ultimately led to the company entering administration in June 2024, suspending all services.

Small World Company operated within the competitive international money transfer market. It competed against established giants and emerging digital platforms. The company's market share and profitability were affected by the rise of digital alternatives and pricing pressures.

The company faced numerous risks, including regulatory changes, financial difficulties, and intense competition. Regulatory fines and increased compliance costs, which rose by an average of 15% in 2024, added to the financial strain. These challenges culminated in the company entering administration.

Given the administration, the immediate future of Small World money transfer is focused on the process and returning funds to customers. The broader financial services industry is focused on technological transformation and strategic partnerships. The industry anticipates a potential increase in M&A activity in 2025.

The money transfer industry faces rapid technological changes, requiring continuous investment in digital platforms. Changing consumer preferences, with a strong trend toward digital payments, pose a challenge. The US mobile payment transactions reached $1.2 trillion in 2024.

Key Takeaways

The Small World Company faced significant challenges, including intense competition and regulatory hurdles. The company's financial difficulties led to its administration in June 2024. The future for the company is uncertain, with the focus on the administration process.

- Intense competition from both established and digital firms.

- Regulatory fines and increasing compliance costs.

- The need for continuous investment in technology to stay competitive.

- The company's administration and suspension of services.

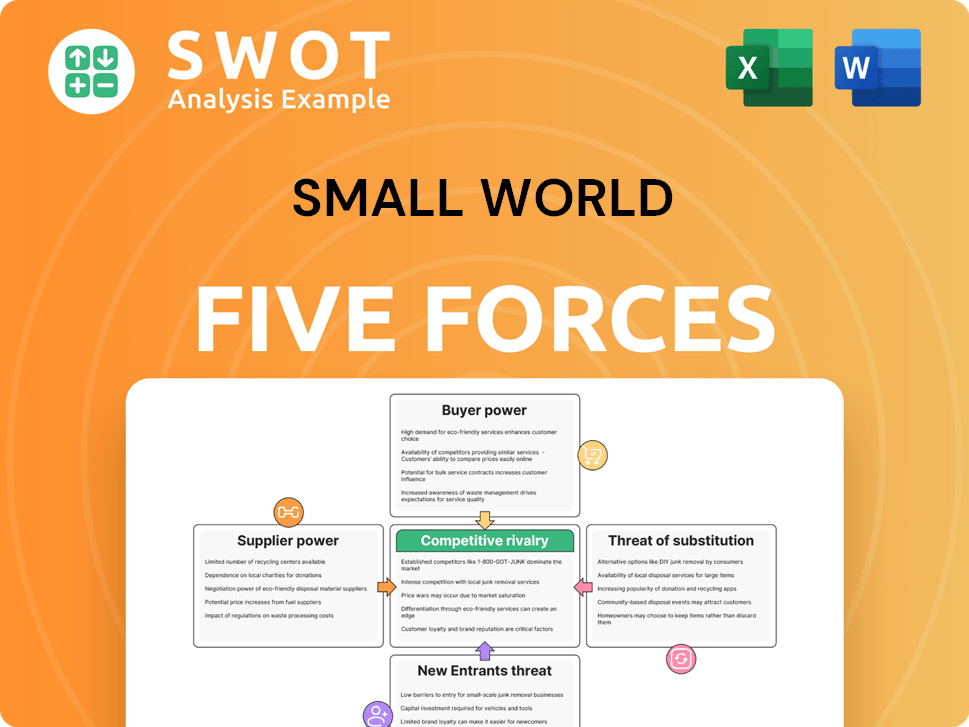

Small World Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Small World Company?

- What is Competitive Landscape of Small World Company?

- What is Growth Strategy and Future Prospects of Small World Company?

- What is Sales and Marketing Strategy of Small World Company?

- What is Brief History of Small World Company?

- Who Owns Small World Company?

- What is Customer Demographics and Target Market of Small World Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.