ICBC Bundle

How Does ICBC, the World's Banking Giant, Operate?

The Industrial and Commercial Bank of China (ICBC) isn't just a bank; it's a global financial ecosystem. As one of the world's largest banks by assets, ICBC's influence permeates international finance and trade. Understanding its operations is crucial for anyone navigating the complexities of the global economy, especially given its systemic importance.

ICBC's vast network and comprehensive services, from traditional banking to investment banking, make it a bellwether for the Chinese economy. For those seeking a deeper understanding of ICBC's strategic positioning, consider exploring the detailed ICBC SWOT Analysis. Whether you're interested in ICBC insurance, navigating ICBC claims, or simply curious about the bank's impact, this analysis offers valuable insights.

What Are the Key Operations Driving ICBC’s Success?

The core operations of ICBC revolve around delivering a broad spectrum of financial products and services to both corporate and retail clients. This includes everything from corporate loans and trade finance to personal loans, mortgages, and credit cards. The bank leverages a vast network of branches, ATMs, and digital platforms to ensure seamless transactions and service delivery. ICBC's operational efficiency is significantly bolstered by its extensive scale and state support, which contribute to its strong competitive position in the domestic market.

For corporate clients, ICBC provides services such as corporate loans, trade finance, and investment banking. Retail customers benefit from personal loans, mortgages, and various deposit services. The bank's operational framework is supported by an extensive branch network, a large ATM presence, and increasingly, robust digital banking platforms, including mobile and online banking. This approach ensures that ICBC can reach a broad demographic and offer convenient access to a wide array of financial services.

ICBC's value proposition centers on offering convenient access to a wide array of financial services, competitive pricing, and the security that comes with being state-backed. The bank's extensive distribution networks, both physical and digital, are unparalleled in China, enabling it to reach a vast customer base. This extensive reach and robust service offerings are key components of ICBC's success.

ICBC provides corporate loans, trade finance, international settlement, cash management, investment banking, and asset management services. These services are designed to support the financial needs of businesses of varying sizes and industries. The bank's focus on corporate clients is a significant part of its overall strategy.

Retail customers benefit from personal loans, mortgages, credit cards, wealth management products, and deposit services. These offerings cater to the diverse financial needs of individual customers. The bank's retail services are designed to be accessible and user-friendly.

ICBC utilizes an extensive branch network, ATMs, and digital platforms, including mobile and online banking. This multi-channel approach ensures broad accessibility and convenience for customers. The bank continuously invests in its digital infrastructure to enhance service delivery.

ICBC's scale and state support provide significant economies of scale and a strong competitive position. This allows the bank to offer competitive pricing and a sense of security to its customers. The bank's strong financial backing is a key differentiator.

Key Operational Strengths

ICBC's operational effectiveness is enhanced by its extensive branch network and digital infrastructure, which facilitate customer acquisition and service. Partnerships with financial institutions and fintech companies expand its global reach. The bank's vast physical presence and digital channels are key to its wide demographic reach.

- Extensive Network: ICBC has a massive physical branch network, particularly within China.

- Digital Innovation: The bank invests heavily in digital banking platforms to enhance customer experience.

- Global Reach: Partnerships with international banks expand ICBC's cross-border capabilities.

- State Support: State backing provides a competitive advantage and enhances financial stability.

ICBC SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does ICBC Make Money?

ICBC's revenue streams are multifaceted, primarily stemming from interest income, fees and commissions, and investment gains. Interest income, a significant portion of its earnings, is derived from its extensive loan portfolio. The bank's diverse financial services generate substantial revenue, with non-interest income playing a crucial role in its financial performance.

The bank strategically monetizes its services through various channels. These include lending activities, generating income from different loan products. Additionally, it utilizes diverse monetization strategies, such as tiered pricing for wealth management products and transaction fees for services like cross-border remittances.

Investment gains also contribute to revenue, though their impact fluctuates with market conditions. Furthermore, ICBC is actively expanding its digital banking services, exploring new monetization avenues through fintech partnerships and digital payment solutions.

Revenue Streams Breakdown

The primary revenue streams for ICBC are interest income, fee and commission income, and investment gains. Interest income, derived from its loan portfolio, is the largest contributor. Fee and commission income comes from various services, and investment gains fluctuate with market conditions.

- Interest Income: As of the end of 2024, ICBC reported a net interest income of approximately RMB 763.5 billion. This income is generated from various loan products, including corporate loans, personal loans, and mortgages.

- Fee and Commission Income: In 2024, ICBC's net fee and commission income reached around RMB 154.9 billion. This income is generated from payment services, credit card fees, wealth management products, and investment banking advisory fees.

- Investment Gains: Investment gains from trading and investment portfolios also contribute to the revenue, though the amount varies based on market performance.

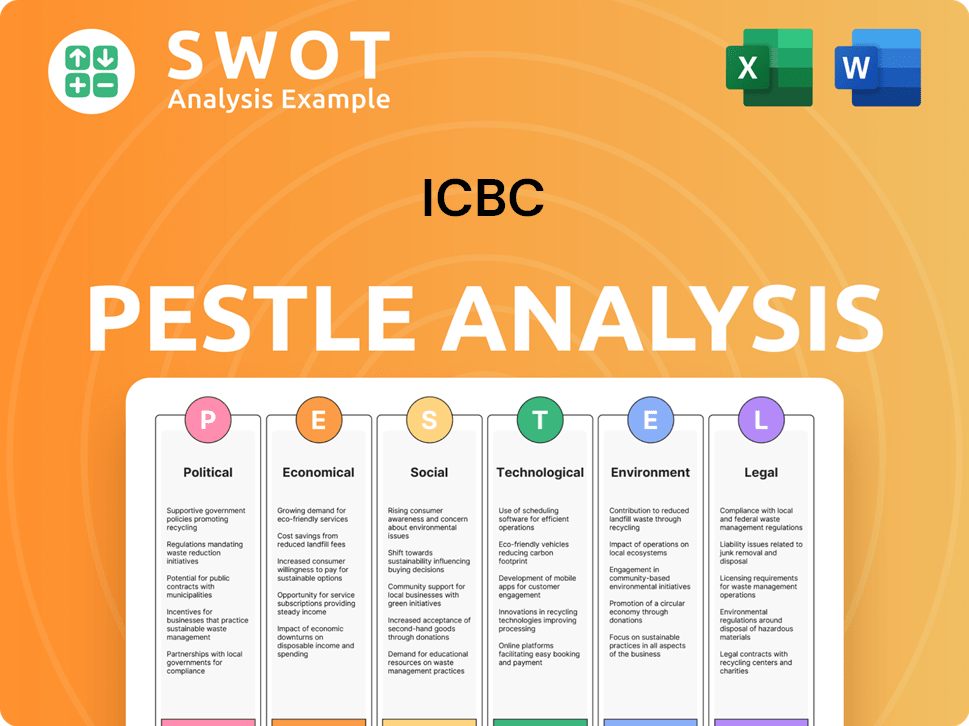

ICBC PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

Which Strategic Decisions Have Shaped ICBC’s Business Model?

ICBC's journey is marked by significant milestones that have solidified its position as a global banking leader. A pivotal strategic move was its dual listing on the Shanghai Stock Exchange and the Hong Kong Stock Exchange in 2006, which was the largest IPO in the world at the time, underscoring its global ambitions. More recently, ICBC has focused on digital transformation, investing heavily in FinTech to enhance its online and mobile banking platforms, a crucial response to evolving customer preferences and the rise of digital competitors.

The bank has also actively participated in China's 'Belt and Road Initiative,' expanding its international footprint and supporting Chinese enterprises' global ventures. Operational challenges have included navigating evolving regulatory landscapes, both domestically and internationally, and managing credit risk in a dynamic economic environment. The bank has responded by strengthening its risk management frameworks and diversifying its loan portfolio. ICBC's competitive advantages are multifaceted, including its unparalleled brand strength and customer trust within China, its vast economies of scale allowing for cost efficiencies, and its extensive branch network providing unmatched reach.

Its strong government backing also provides a significant competitive edge, fostering stability and confidence. ICBC continues to adapt to new trends, such as the increasing demand for green finance and sustainable investments, by developing relevant products and services, aiming to maintain its leadership in a rapidly changing financial world. For those interested in understanding the competitive environment, information about ICBC's competitors can offer additional insights.

ICBC's dual listing in 2006 on the Shanghai and Hong Kong Stock Exchanges was a landmark event, representing the world's largest IPO at the time. This strategic move significantly boosted its global presence and financial capacity. The bank's expansion through the 'Belt and Road Initiative' further enhanced its international footprint, supporting Chinese enterprises' global ventures.

ICBC has prioritized digital transformation to meet changing customer needs, investing heavily in FinTech to improve its online and mobile banking platforms. The bank actively manages credit risk and adapts to regulatory changes. ICBC has also expanded its green finance offerings, aligning with the growing demand for sustainable investments.

ICBC benefits from strong brand recognition and customer trust within China, along with extensive economies of scale. Its vast branch network provides unmatched reach, and strong government backing offers a significant competitive advantage. ICBC's ability to adapt to new trends, such as green finance, further strengthens its market position.

ICBC faces challenges in navigating evolving regulatory landscapes both domestically and internationally. Managing credit risk in a dynamic economic environment is another key operational challenge. The bank addresses these issues by strengthening its risk management frameworks and diversifying its loan portfolio.

ICBC's Financial Performance and Market Position

In recent years, ICBC has shown consistent financial growth, with its total assets reaching approximately $6.7 trillion USD as of 2024. The bank's net profit for 2024 was around $55 billion USD, demonstrating its strong profitability. ICBC's market capitalization places it among the largest banks globally, reflecting its significant influence in the financial sector.

- ICBC's global network includes thousands of branches and offices worldwide.

- The bank's focus on digital transformation has led to a significant increase in online and mobile banking usage.

- ICBC's involvement in the 'Belt and Road Initiative' has expanded its international lending portfolio.

- The bank continues to invest in green finance initiatives, supporting sustainable development projects.

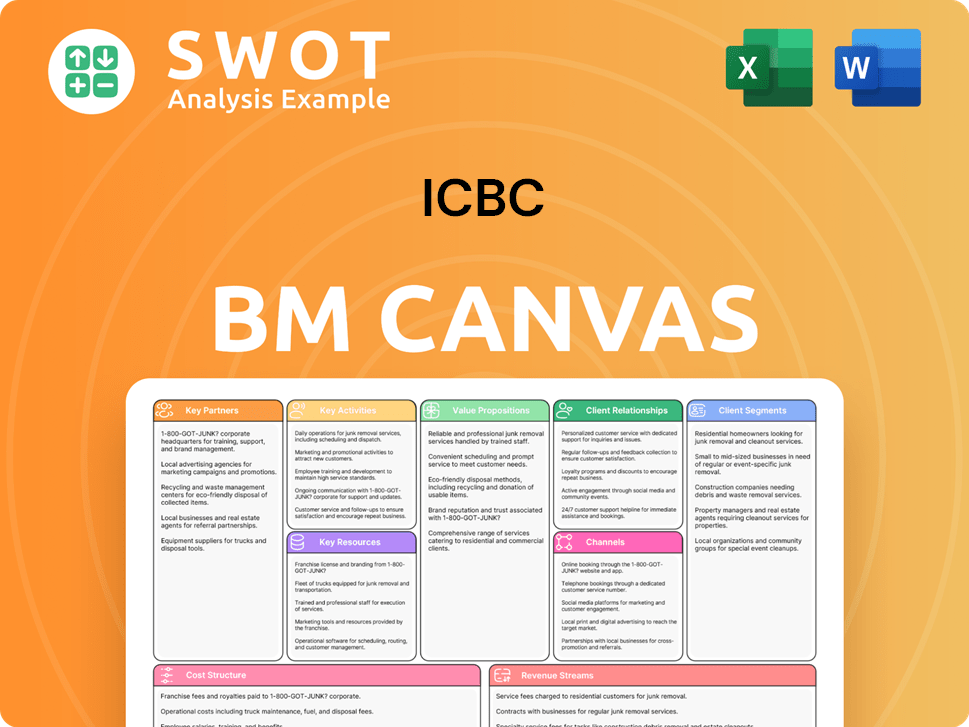

ICBC Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

How Is ICBC Positioning Itself for Continued Success?

As a global banking leader, ICBC holds a prominent position, consistently ranking among the world's largest banks by assets. Its significant market share in China, coupled with a vast and loyal customer base, particularly benefits from its extensive network and perceived stability. ICBC's international presence supports cross-border activities, solidifying its role in the global financial system.

However, ICBC faces various challenges. Regulatory changes, competition from fintech companies, and technological advancements require continuous adaptation. Changing consumer preferences and the need for digital and personalized services also push for ongoing innovation. To mitigate these risks, ICBC invests in digital transformation, expands green finance offerings, and strengthens risk management.

ICBC is a dominant player in the global banking sector, known for its substantial assets and wide-reaching influence. It maintains a strong presence in China and has expanded its international footprint. The bank's large customer base and extensive network contribute to its strong market position, making it a key player in international finance.

ICBC faces risks from regulatory changes, competition from fintech companies, and rapid technological advancements. These factors necessitate continuous investment and adaptation to stay competitive. Changing consumer preferences and the need for digital services also pose challenges. The bank is actively working to mitigate these risks through strategic initiatives.

The future outlook for ICBC involves leveraging its strong foundation and strategic investments to sustain revenue growth. This includes adapting to market dynamics, embracing technological advancements, and continuing to serve as a cornerstone of the global financial system. ICBC is committed to sustainable growth and international expansion.

ICBC is focusing on digital transformation, expanding green finance offerings, and strengthening risk management. These initiatives are designed to enhance its competitive position and support sustainable growth. Leadership emphasizes a commitment to innovation and international expansion to navigate the evolving financial landscape.

Key Considerations for ICBC

ICBC's success hinges on its ability to navigate regulatory changes and adapt to technological advancements. The bank must also meet evolving customer expectations for digital and personalized services. To understand how ICBC approaches its marketing strategy, you can read more in the Marketing Strategy of ICBC.

- Digital Transformation: Investing in technology to improve services.

- Green Finance: Expanding green finance offerings to support sustainability.

- Risk Management: Strengthening risk management frameworks.

- Customer Focus: Adapting to changing consumer preferences.

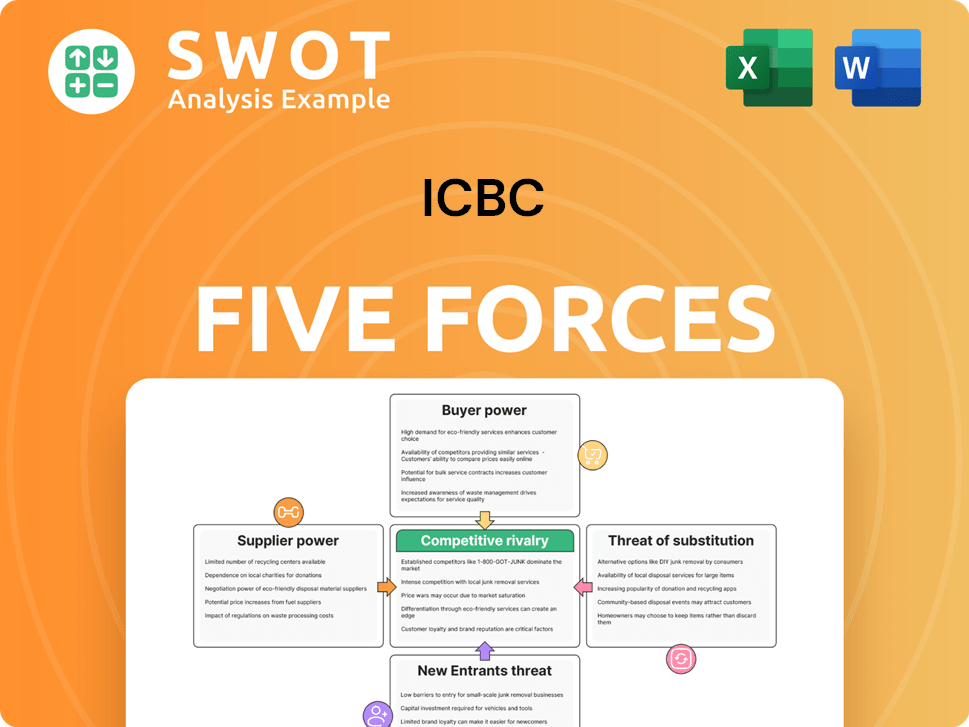

ICBC Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of ICBC Company?

- What is Competitive Landscape of ICBC Company?

- What is Growth Strategy and Future Prospects of ICBC Company?

- What is Sales and Marketing Strategy of ICBC Company?

- What is Brief History of ICBC Company?

- Who Owns ICBC Company?

- What is Customer Demographics and Target Market of ICBC Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.