Ujjivan Bundle

Can Ujjivan SFB Continue Its Impressive Growth Trajectory?

Ujjivan Small Finance Bank (SFB) has rapidly expanded its footprint in India's financial sector, focusing on financial inclusion since its inception in 2005. From its origins as a microfinance institution to its current status with 752 branches, Ujjivan SFB has demonstrated a commitment to serving underserved communities. With a substantial customer base and a robust loan and deposit portfolio, Ujjivan SFB is a compelling case study in sustainable financial growth.

To understand the future, it's crucial to dissect Ujjivan's Ujjivan SWOT Analysis, which reveals its strengths, weaknesses, opportunities, and threats. The Ujjivan Growth Strategy is built on expansion, technological innovation, and sound financial management, aiming to deepen its market penetration and diversify its offerings. This analysis will delve into Ujjivan's Financial Performance, Business Model, and Market Position, providing insights into its competitive landscape and long-term growth outlook.

How Is Ujjivan Expanding Its Reach?

To understand the Ujjivan Growth Strategy and its Future Prospects, it's crucial to examine the expansion initiatives the bank is undertaking. These initiatives are designed to diversify its portfolio, broaden its geographical reach, and enhance its service offerings. The bank's strategic moves are aimed at solidifying its market position and driving sustainable growth in the competitive financial landscape.

Ujjivan Company Analysis reveals a strong focus on adapting to market dynamics and customer needs. The bank's approach involves a shift in its lending strategy, geographical expansion, and the introduction of new products and services. These efforts are geared towards increasing profitability and providing a wider range of financial solutions to its customers. The bank is also focusing on improving its housing loan product, prioritizing accessibility and streamlining turnaround times, and has ventured into capital market services, including demat services and exploring mutual fund offerings.

The bank's strategic initiatives are well-defined and data-driven, indicating a proactive approach to growth and market penetration. By analyzing these expansion plans, investors and stakeholders can gain valuable insights into Ujjivan's Future Investment Opportunities and its potential for long-term success. For more details on the bank's core values, you can read Mission, Vision & Core Values of Ujjivan.

One of the primary strategies involves diversifying the loan portfolio. This includes reducing the reliance on microfinance loans and increasing the share of secured loans. As of December 2024, the microfinance loan share was at 61%, down from 70% in March 2024.

Secured loans, encompassing housing, MSME, vehicle finance, and gold loans, are projected to grow significantly. These loans are expected to grow at a CAGR of over 20% in the next five years. This strategic shift aims to balance risk and enhance profitability.

The bank plans to expand its gold loan offerings. The goal is to have gold loans available at 250 branches by the end of the current financial year. This is a substantial increase from the current 60 branches.

Geographical expansion is a key element of the growth strategy. Ujjivan added 123 branches in FY24, bringing the total to 752 across 26 states. The bank plans to add 50 more branches in FY25 to broaden its reach.

Enhancing Service Offerings

Ujjivan is focused on enhancing its service offerings to attract and retain customers. This includes launching new product lines and improving existing ones.

- Working Capital Offerings: Launching fund-based and non-fund-based working capital offerings across the country.

- Housing Loans: Improving the housing loan product by prioritizing accessibility and streamlining turnaround times.

- Capital Market Services: Venturing into capital market services, including demat services and exploring mutual fund offerings.

- CASA Deposits: Expanding into major urban centers to capitalize on low-cost current and savings account (CASA) deposits.

Ujjivan SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Ujjivan Invest in Innovation?

The innovation and technology strategy of Ujjivan Small Finance Bank is critical for its Ujjivan Growth Strategy and future success. Their focus on digital transformation aims to enhance customer experiences and streamline operations. This approach is essential for maintaining a strong Ujjivan Market Position.

Ujjivan is heavily investing in technology to drive financial inclusion and cater to a diverse customer base. By leveraging digital channels, the bank seeks to expand its reach and offer convenient services. This strategy supports Ujjivan's Expansion Plans and long-term growth.

As of July 2024, a significant 89.79% of Ujjivan's transactions are digital, reflecting a strong shift towards online banking. This digital focus is key to the bank's Ujjivan Future Prospects and its ability to compete effectively in the market.

Digital Transformation Initiatives

Ujjivan is upgrading its mobile and internet banking platforms. This upgrade aims to provide a wider range of services. The goal is to attract more customers to digital channels.

'Hello Ujjivan' Mobile App

The 'Hello Ujjivan' app is designed for semi-literate and rural customers. It uses AI and machine learning for voice, visual, and vernacular features. The app is available in ten regional languages and English.

Robotic Process Automation (RPA)

Ujjivan has implemented RPA to automate 41 processes. This automation improves customer service and reduces turnaround time. It streamlines operations and enhances efficiency.

AI and Predictive Analytics

The bank is exploring AI for fraud detection and predictive analytics. An early warning system uses AI to predict non-performing assets (NPAs). This helps in proactive risk management.

Digital Offerings

Ujjivan offers end-to-end digital savings and fixed deposits. Customers can open accounts online with video KYC. This enhances convenience and accessibility.

Fintech Partnerships

The bank collaborates with fintech partners to enhance outreach and service delivery. These partnerships help expand the bank's reach. This strategy supports Ujjivan's Strategic Partnerships and Collaborations.

Ujjivan's investment in technology directly impacts its Ujjivan Financial Performance and ability to adapt to market changes. The bank's digital initiatives are designed to improve customer experience and operational efficiency. These efforts are critical for long-term sustainability and growth. For more insights, see Target Market of Ujjivan.

Key Technological Advancements

Ujjivan is focused on integrating advanced technologies to enhance its services and operations. This includes AI, RPA, and digital platforms. These technologies are crucial for improving efficiency and customer satisfaction.

- AI for Fraud Detection: Implementing AI to identify and prevent fraudulent activities.

- Predictive Analytics for NPAs: Using AI to forecast and manage non-performing assets.

- Voice-Enabled Banking: Offering services in multiple languages for wider accessibility.

- RPA for Automation: Automating processes to reduce manual effort and improve turnaround times.

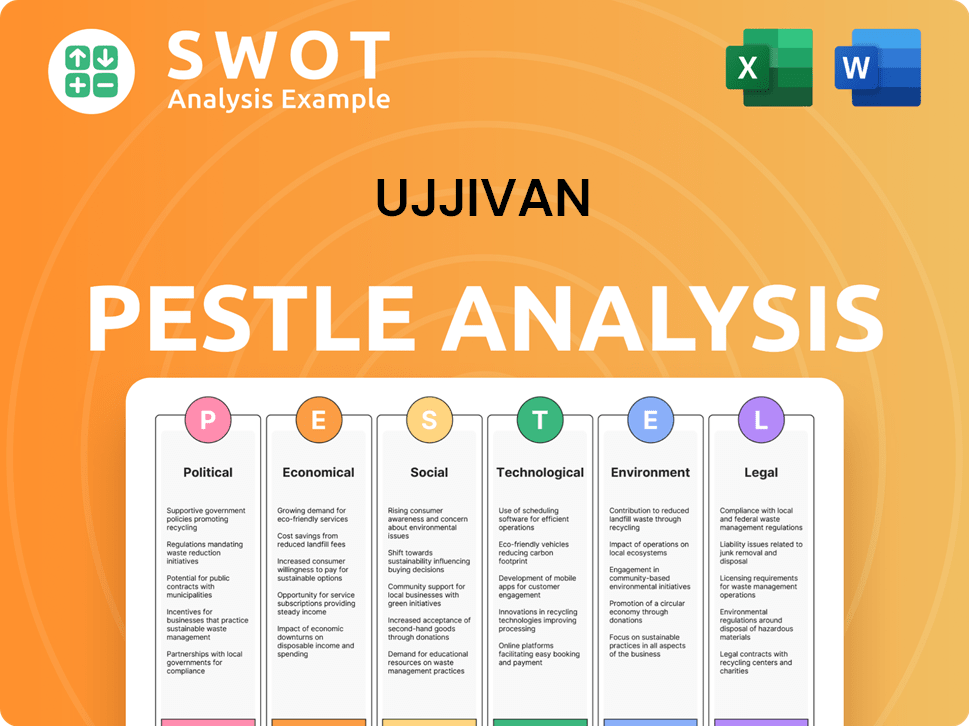

Ujjivan PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Ujjivan’s Growth Forecast?

The financial outlook for Ujjivan Small Finance Bank (USFB) presents a mixed picture, blending strong growth in some areas with challenges that have impacted profitability. Understanding the Ujjivan Growth Strategy requires a close examination of its recent performance and future projections.

For the fiscal year 2024-25 (FY25), Ujjivan reported a net profit of ₹726 crore, a decrease from ₹1,281.50 crore in FY24. This decline was partially offset by an increase in total income, which rose to ₹7,201 crore in FY25 from ₹6,464 crore the previous year. The bank's Ujjivan Financial Performance reflects both the resilience and the hurdles it faces in the current economic climate.

In the fourth quarter of FY25 (Q4 FY25), the net profit experienced a significant drop of 75% year-on-year, reaching ₹83.39 crore. This decrease was primarily attributed to higher provisions for bad loans. Despite this, the bank's revenue for Q4 FY25 saw a 4.44% year-on-year increase, reaching ₹1,843.05 crore. These figures are crucial for a thorough Ujjivan Company Analysis.

The gross loan book reached ₹30,466 crore as of December 2024, showing a 9.8% year-on-year growth. Deposits also grew by 16.3% year-on-year to ₹34,494 crore as of December 2024. This growth indicates a strong customer base and effective deposit mobilization strategies.

The bank maintained a robust capital adequacy ratio (CAR) of 23.90% as of December 31, 2024. This strong capital position provides a solid foundation for future business expansion and helps manage potential risks effectively.

Ujjivan has adjusted its FY25 loan growth guidance to approximately 20% year-on-year, down from the earlier expectation of 25%. This reflects a cautious approach, acknowledging building stress in some business segments. This adjustment is critical for understanding Ujjivan Future Prospects.

The bank anticipates a return on equity (ROE) of 22% and credit costs of 1.7% for FY25. These figures are crucial for assessing the bank's profitability and risk management capabilities. Understanding the risk management approach is essential for investors.

Analyst Projections

Analysts project that by FY27, Ujjivan's net profit could increase to ₹1,459 crore, with the balance sheet expanding to ₹70,560 crore. These projections highlight the potential for significant growth in the coming years. For more insights into the bank's strategies, you can read about the Marketing Strategy of Ujjivan.

- The bank's ability to manage credit costs will be crucial.

- Deposit growth remains a key driver for balance sheet expansion.

- Maintaining a strong capital base is essential for sustained growth.

- The bank's focus on digital transformation is important.

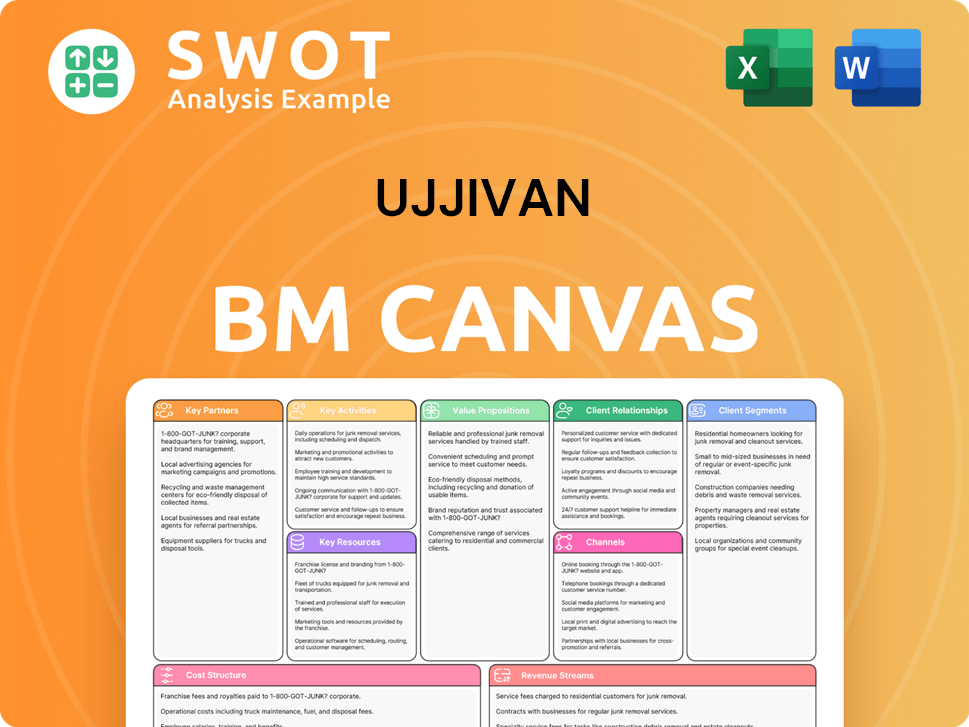

Ujjivan Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Ujjivan’s Growth?

The growth strategy and future prospects of the Ujjivan Small Finance Bank are subject to several potential risks and obstacles. These challenges span operational, financial, and strategic areas, which could influence its ability to achieve its growth targets. Understanding these risks is crucial for a comprehensive Ujjivan Company Analysis.

A significant portion of Ujjivan's loan portfolio is concentrated in the microfinance sector. This concentration exposes the bank to risks such as socio-political interference and regulatory changes. The bank's asset quality has also been a concern, with rising non-performing assets (NPAs) impacting financial performance. This situation requires careful monitoring and proactive risk management.

Intense competition and economic downturns pose additional threats to Ujjivan's growth. The bank's customer base, which includes economically weaker sections, is particularly vulnerable to economic fluctuations. Operational risks related to cash transactions and data security in digital banking are also present. Effective mitigation strategies are essential for sustainable growth.

Microfinance Sector Risks

The microfinance sector, constituting a large portion of Ujjivan's loan book, is prone to socio-political interventions and regulatory uncertainties, impacting the bank's operations. Risks include the challenges associated with unsecured lending, affecting asset quality and overall financial stability. These factors require continuous monitoring and strategic adjustments.

Asset Quality Concerns

Ujjivan's asset quality has shown signs of stress, with Gross Non-Performing Assets (GNPA) increasing to 2.68% as of December 31, 2024, from 2.23% on March 31, 2024. This increase, coupled with significant write-offs and sales of NPAs, highlights the need for robust asset quality management. Slippages are expected to remain elevated, posing a challenge to Ujjivan's Financial Performance.

Competitive Pressures and Economic Slowdowns

Ujjivan faces intensified competition from new players in the small finance segment. Economic slowdowns, particularly in rural regions, could constrain growth. The bank must navigate these challenges by diversifying its portfolio and focusing on cost optimization to maintain its market position.

Regulatory and Operational Risks

Regulatory uncertainties and shifts in policies can impact Ujjivan's profitability and operations. Operational risks, such as those related to cash-based transactions and the critical need for customer data privacy and security in digital banking, are also significant. Addressing these risks is crucial for sustained growth.

Portfolio Diversification and Risk Mitigation

Ujjivan is diversifying its product portfolio towards secured loans to mitigate risks. The bank's focus on asset quality management, cost optimization, and profitability enhancement are key strategies. Implementing a Board-approved Stress Testing policy and framework is vital for assessing vulnerability to stressed business conditions.

Customer Base Vulnerability

The majority of the non-microfinance retail segment consists of economically weaker sections and low-income groups, making Ujjivan vulnerable to economic downturns. Strategies to support this customer base during economic challenges are essential for maintaining financial stability and Ujjivan's Business Model.

Ujjivan's strategies to mitigate risks include diversifying its product portfolio, focusing on asset quality management, cost optimization, and profitability enhancement. The bank has implemented a Board-approved Stress Testing policy to assess its vulnerability to stressed business conditions. These initiatives are crucial for navigating the challenges and realizing Ujjivan's Future Prospects.

The bank addresses risks through measures like diversifying its product portfolio, focusing on asset quality management, cost optimization, and profitability enhancement. It has also implemented a Board-approved Stress Testing policy and framework to assess vulnerability to extreme but plausible stressed business conditions. This approach is critical for ensuring long-term financial health.

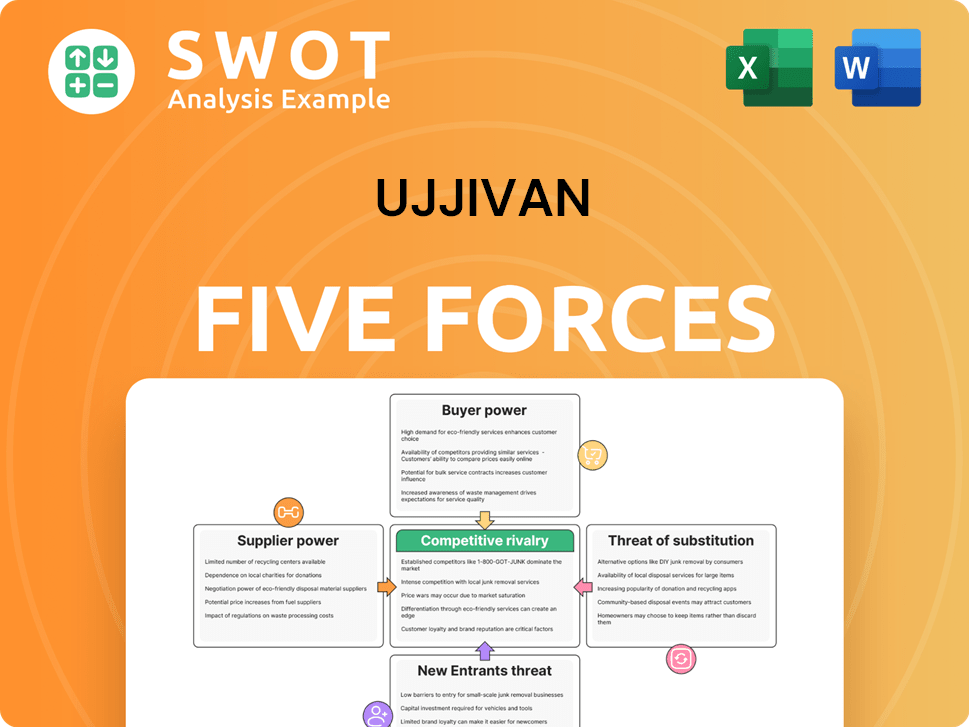

Ujjivan Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Ujjivan Company?

- What is Competitive Landscape of Ujjivan Company?

- How Does Ujjivan Company Work?

- What is Sales and Marketing Strategy of Ujjivan Company?

- What is Brief History of Ujjivan Company?

- Who Owns Ujjivan Company?

- What is Customer Demographics and Target Market of Ujjivan Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.